This site displays a prototype of a “Web 2.0” version of the daily Federal Register. It is not an official legal edition of the Federal Register, and does not replace the official print version or the official electronic version on GPO’s govinfo.gov.

The documents posted on this site are XML renditions of published Federal Register documents. Each document posted on the site includes a link to the corresponding official PDF file on govinfo.gov. This prototype edition of the daily Federal Register on FederalRegister.gov will remain an unofficial informational resource until the Administrative Committee of the Federal Register (ACFR) issues a regulation granting it official legal status. For complete information about, and access to, our official publications and services, go to About the Federal Register on NARA's archives.gov.

The OFR/GPO partnership is committed to presenting accurate and reliable regulatory information on FederalRegister.gov with the objective of establishing the XML-based Federal Register as an ACFR-sanctioned publication in the future. While every effort has been made to ensure that the material on FederalRegister.gov is accurately displayed, consistent with the official SGML-based PDF version on govinfo.gov, those relying on it for legal research should verify their results against an official edition of the Federal Register. Until the ACFR grants it official status, the XML rendition of the daily Federal Register on FederalRegister.gov does not provide legal notice to the public or judicial notice to the courts.

- Regulations.gov DataEnhanced Content - Regulations.gov Data

FederalRegister.gov retrieves relevant information about this document from Regulations.gov to provide users with additional context. This information is not part of the official Federal Register document.

Reimagining and Improving Student Education (RISE) Committee

- Docket ID

- ED-2025-OPE-0944

- Supporting Documents

- Information Collection Requirement: Forms and Instruments

- Information Collection Requirement: Supporting Statement

AGENCY:

Office of Postsecondary Education, Department of Education.

ACTION:

Notice of proposed rulemaking.

SUMMARY:

The Secretary proposes to amend the regulations for the Federal student loan programs authorized under title IV of the Higher Education Act (HEA) of 1965, as amended (the title IV, HEA programs) to implement the statutory changes to the title IV, HEA programs included in the One Big Beautiful Bill Act (OBBB) signed into law by President Trump on July 4, 2025. These changes include establishing new loan limits for graduate students, professional students, and parents, and phasing out the Graduate PLUS Program. The Department notes that the term “professional student” as used in this Notice of Proposed Rulemaking (NPRM) is intended solely to distinguish those programs that we propose would be eligible for higher loan limits, as required by the OBBB. The designation, or lack thereof, of a program as “professional” does not reflect a value judgment by the Department regarding whether a borrower graduating from the program is considered a “professional.” This NPRM only interprets the phrase “professional student” as used in the context of the loan limits established by the OBBB. The OBBB also simplifies the current broken and confusing myriad of Federal student loan repayment plans by phasing out the existing Income-Contingent Repayment (ICR) plans, creating a new tiered standard repayment plan option, and implementing a new income-driven repayment plan known as the Repayment Assistant Plan. The OBBB also enables borrowers in default who have previously rehabilitated a defaulted loan a second chance to rehabilitate their loan(s) and resume repayment.

DATES:

We must receive your comments on or before March 2, 2026.

ADDRESSES:

Submit your comments through the Federal eRulemaking Portal at www.regulations.gov. The Department of Education (Department) will not accept comments submitted by fax or by email or comments submitted after the comment period closes. To make sure that the Department does not receive duplicate copies, please submit your comment only once. Additionally, please include the Docket ID at the top of your comments.

Information on using Regulations.gov, including instructions for submitting comments, is available on the site under “FAQ.” If you require an accommodation or cannot otherwise submit your comments via Regulations.gov, please contact regulationshelpdesk@gsa.gov or by phone at 1-866-498-2945. If you are deaf, hard of hearing, or have a speech disability and wish to access telecommunications relay services, please dial 7-1-1.

Privacy Note: The Department's policy is to make all comments received from members of the public available for public viewing in their entirety on the Federal eRulemaking at www.regulations.gov. Therefore, commenters should include in their comments only information that they wish to make publicly available. Additionally, commenters should not include in their comments any personally identifiable information (PII) in comments about other individuals. For example, if your comment describes an experience of someone other than yourself, please do not identify that individual or include any personal information that identifies that individual. The Department reserves the right to redact a portion of a comment or the entire comment at any time if any PII about other individuals is included.

FOR FURTHER INFORMATION CONTACT:

Tamy Abernathy, Office of Postsecondary Education, 400 Maryland Ave. SW, 5th Floor, Washington, DC 20202. Telephone: (202) 245-4595. Email: NegRegNPRMHelp@ed.gov.

SUPPLEMENTARY INFORMATION:

I. Executive Summary

The Secretary proposes to implement the amendments made to the HEA relating to the Federal student loan programs made by the OBBB through these regulations.

These proposed regulations would revise the Direct Loan Program under 34 CFR part 685 by amending annual and aggregate loan limits for graduate, professional, and parent loan borrowers. The proposed regulations would also implement two new streamlined student loan repayment plans for new borrowers, the “Repayment Assistance Plan” and the “Tiered Standard” repayment plan. The proposed regulations also make conforming amendments to current regulations on consolidation, deferment, forbearance, and Public Service Loan Forgiveness (PSLF). The proposed regulations also provide borrowers in default a second opportunity to rehabilitate their loans and resume repayment, even if they previously rehabilitated a defaulted loan.

A brief summary of these proposed regulations is available at https://www.regulations.gov/document/ED-2025-OPE-0944.

II. Summary of the Major Provisions of This Regulatory Action

These proposed regulations would:

- Amend §§ 674.39, 682.215, and 682.405 to allow loan rehabilitation twice per each loan borrowed under the Federal Perkins Program, Federal Family Education Loan Program, and the Direct Loan Program.

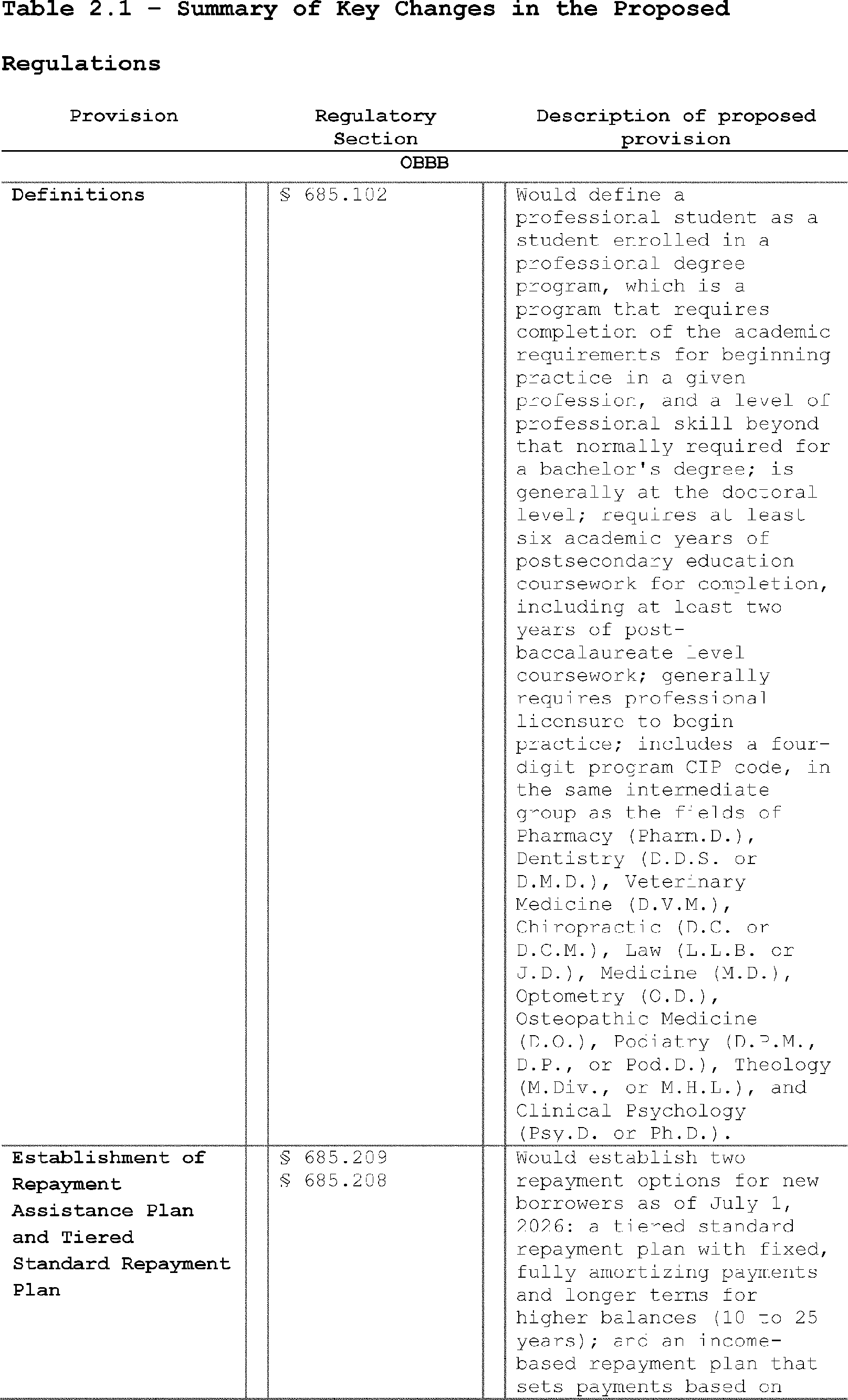

- Amend § 685.102 to include new definitions for the following terms:expected time to credential, graduate student,professional student, and program length.

- Amend § 685.200 to include Direct PLUS Loan eligibility for graduate and professional students.

- Amend § 685.201 to establish the limited Direct PLUS Loan eligibility for a graduate or professional student.

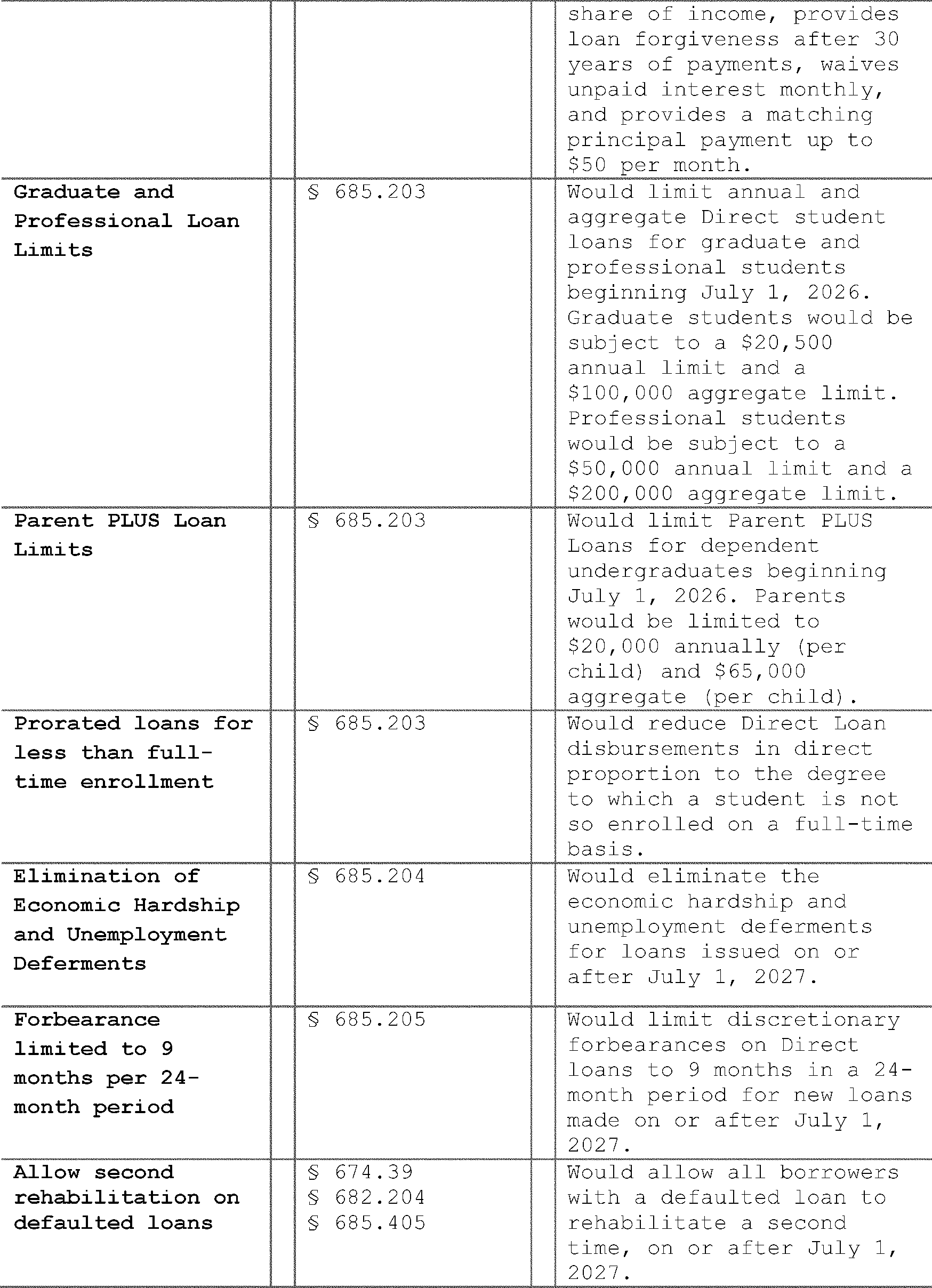

- Amend § 685.203 to include new Direct Loan annual and aggregate limits, create a new lifetime maximum aggregate limit, establish less than full-time reduction of annual loan limits, and permit institutions to limit borrowing for specific programs.

- Amend § 685.204 to clarify conditions and borrower eligibility for the unemployment deferment and the economic hardship deferment.

- Amend § 685.205 to establish the modified eligibility criteria for borrowers to receive a forbearance.

- Amend § 685.208 to establish the terms for the Tiered Standard repayment plan, set the minimum payment for the Tiered Standard repayment plan, and restructure each Fixed repayment plan's terms under their respective plan.

- Amend § 685.209 to establish terms for the Repayment Assistance Plan and sunset ICR plans and conditions.

- Amend § 685.210 to provide information to borrowers about choosing a repayment plan.

- Amend § 685.211 to establish miscellaneous repayment provisions including the minimum payment increase for the Income-Based Repayment (IBR) plan.

- Amend § 685.219 to clarify that repaying under the Repayment Assistance Plan will qualify for PSLF if all other eligibility criteria are met.

- Amend § 685.220 to provide terms and repayment plan eligibility for consolidation loans. ( printed page 4255)

- Amend § 685.221 to clarify when a borrower may be eligible for an alternative repayment plan.

- Amend § 685.303 to waive the substantially equal disbursement requirement for an institution when a borrower has less than full-time enrollment for the academic year and is subject to the schedule of reductions.

While the Department is proposing the regulations in a consolidated NPRM, it considers each to be a discrete change independent of other proposed changes. Consistent with 34 CFR 685.109, “[i]f any provision of this subpart or its application to any person, act, or practice is held invalid, the remainder of the subpart or the application of its provisions to any person, act, or practice will not be affected thereby.”

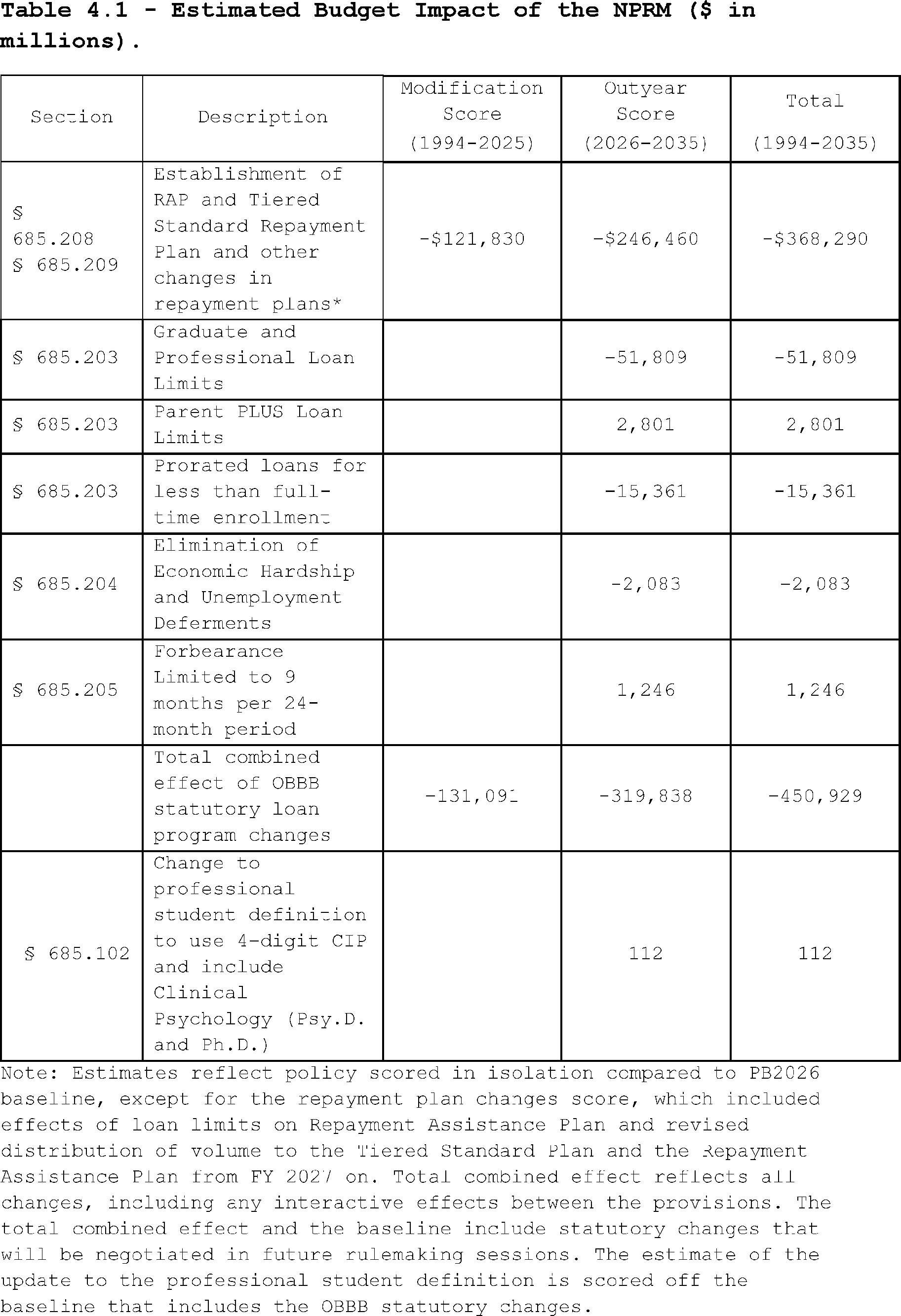

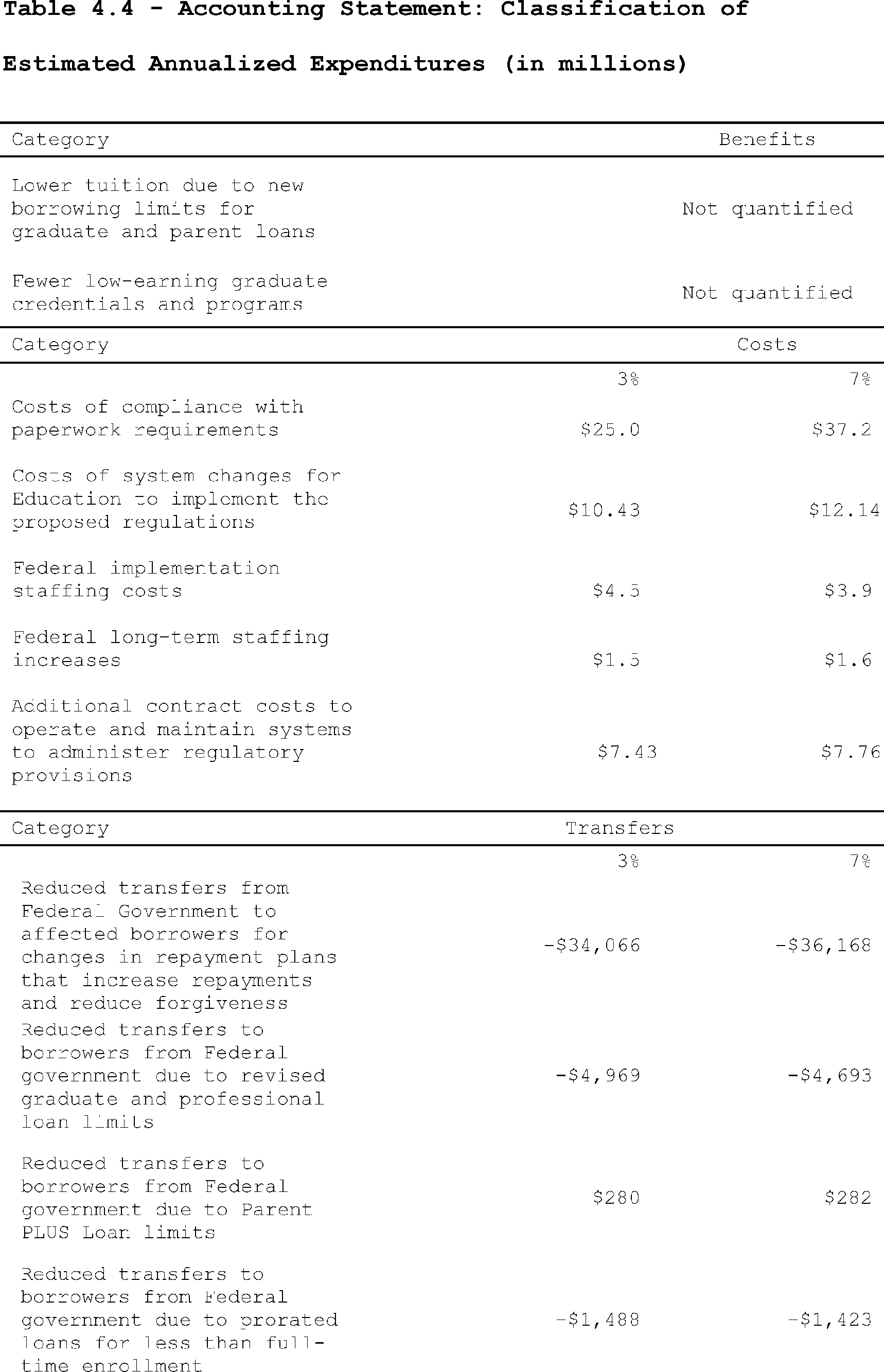

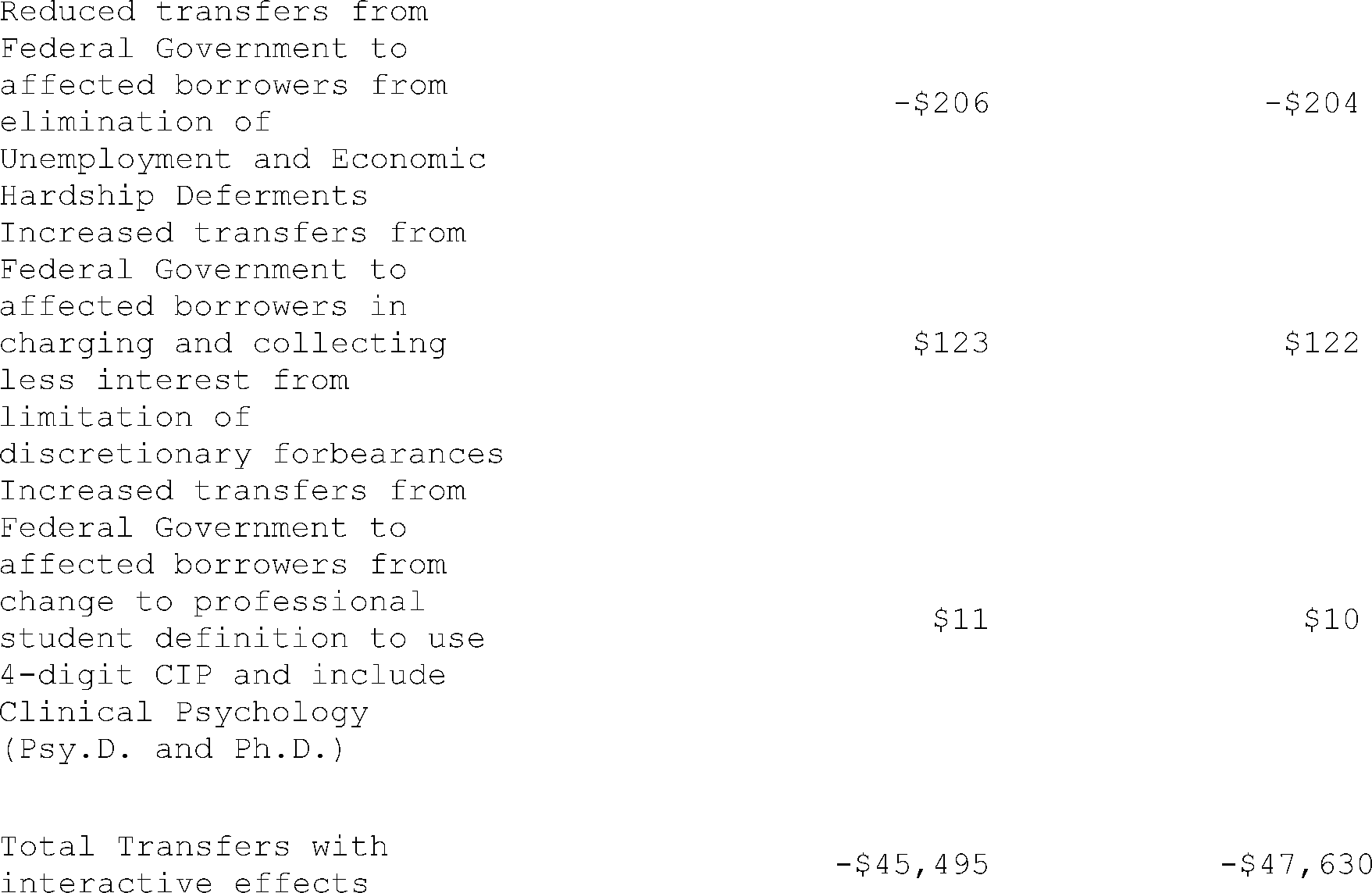

Cost and Benefits:

As further detailed in the Regulatory Impact Analysis (RIA), the proposed regulations would have significant impacts on students, borrowers, educational institutions, and taxpayers.

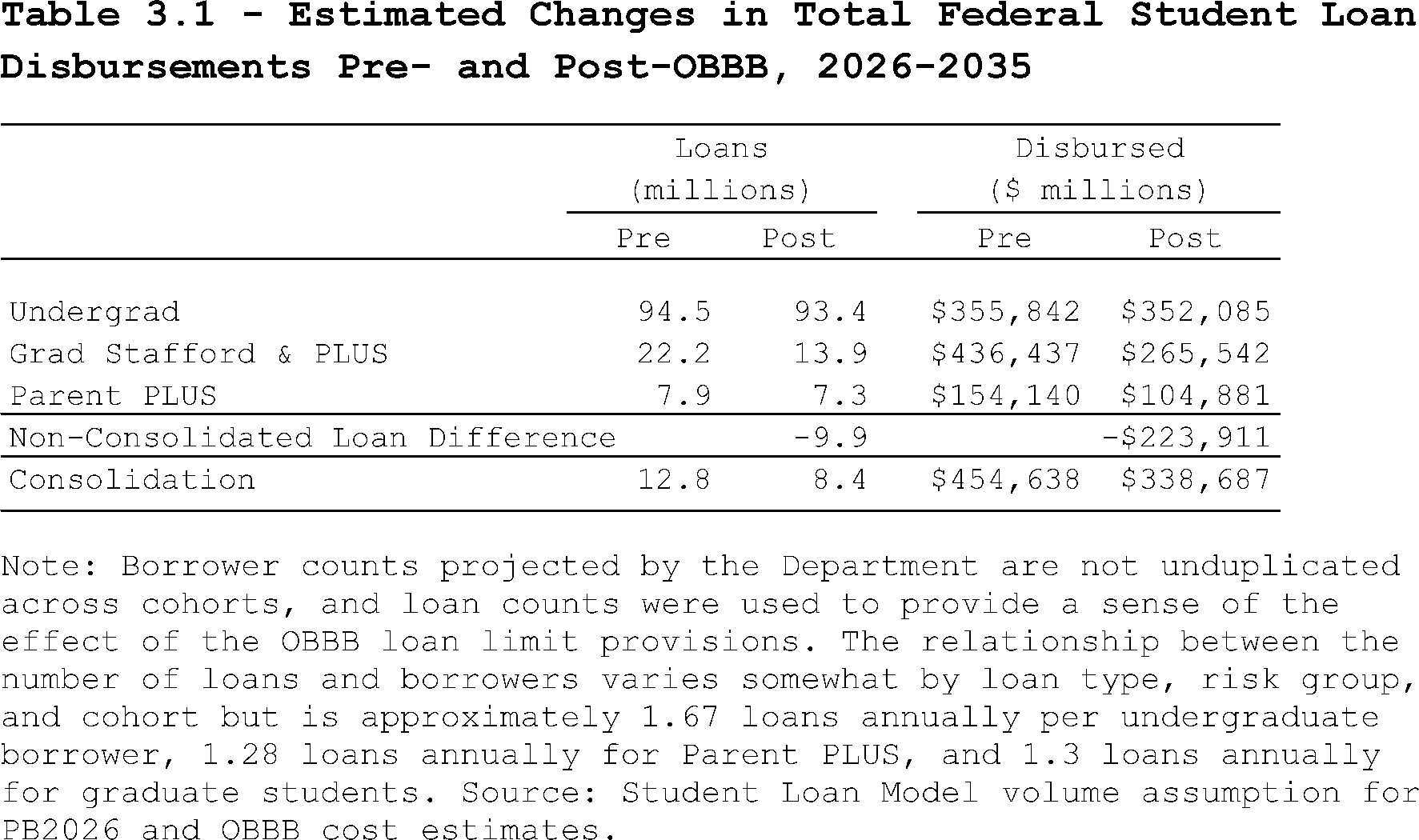

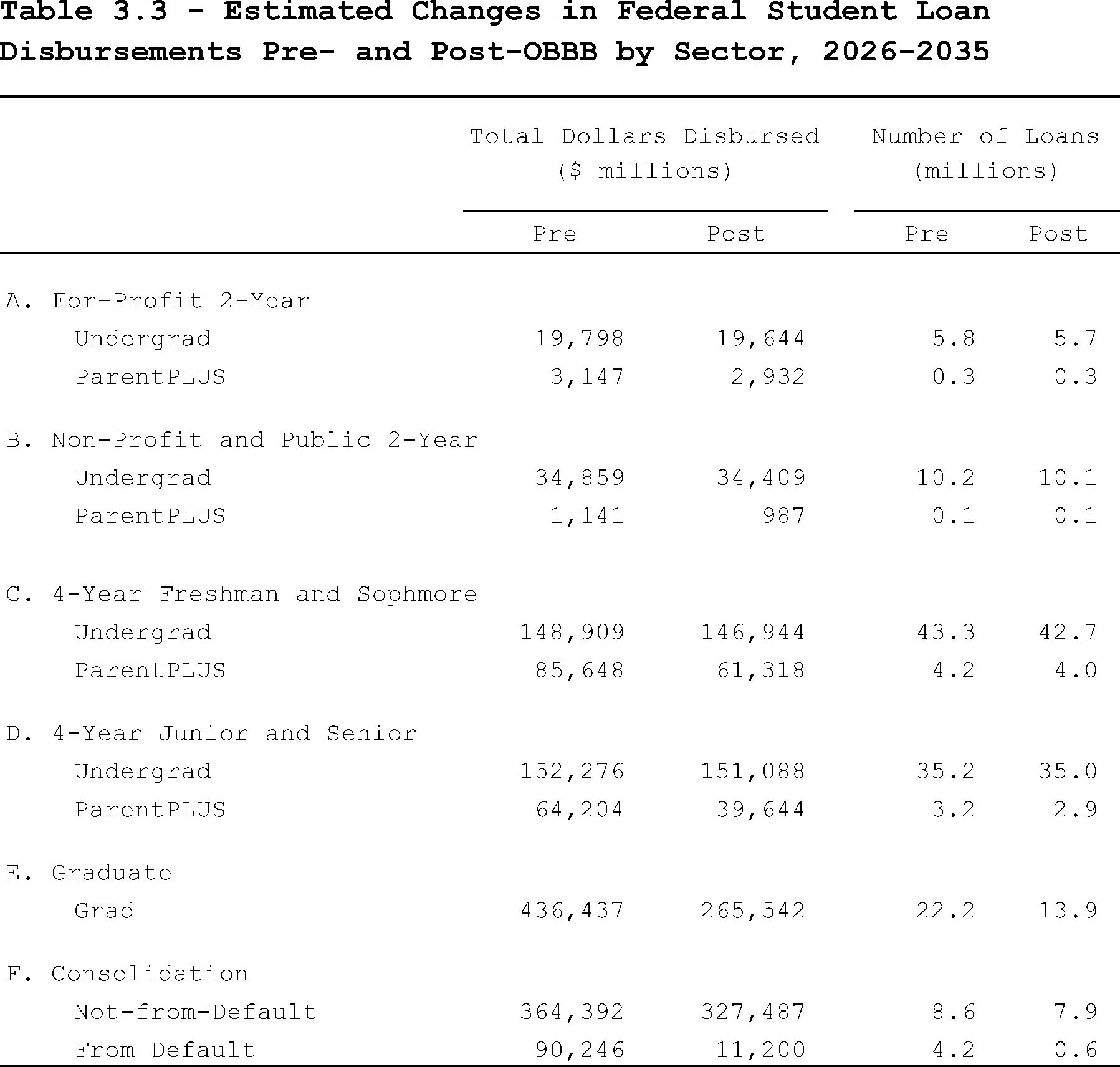

Under the proposed revisions, borrowers would benefit from new loan repayment terms, such as monthly interest cancellation and principal payment subsidies under the Repayment Assistance Plan. New caps on Federal loans for graduate and professional education, as well as caps on Parent PLUS Loans, will rein in increases in graduate student and parent borrowing and put downward pressure on tuition prices at institutions. These new loan limits will encourage institutions to evaluate the true cost of their programs and create efficiencies where necessary to allow students to enroll and fund their education within the boundaries of the new, responsible, loan limits determined by Congress and/or the institution. Changes to student loans enacted in the OBBB will result in significant savings to the taxpayer by reducing the excessive subsidy costs of loan forgiveness and other high-cost terms and conditions. Specifically, the new annual and lifetime caps on borrowing will reduce taxpayer exposure for loans that could potentially be forgiven under the Department's Public Service Loan Forgiveness Program, Closed School Loan Discharges, Borrower Defense to Repayment discharges, death of the borrower discharges, total and permanent disability discharges, time-based forgiveness discharges under income-based repayment, and discharges that may occur in bankruptcy. The Department estimates that from 2021 to 2025, it forgave $199 billion in student debt as a result of these provisions.

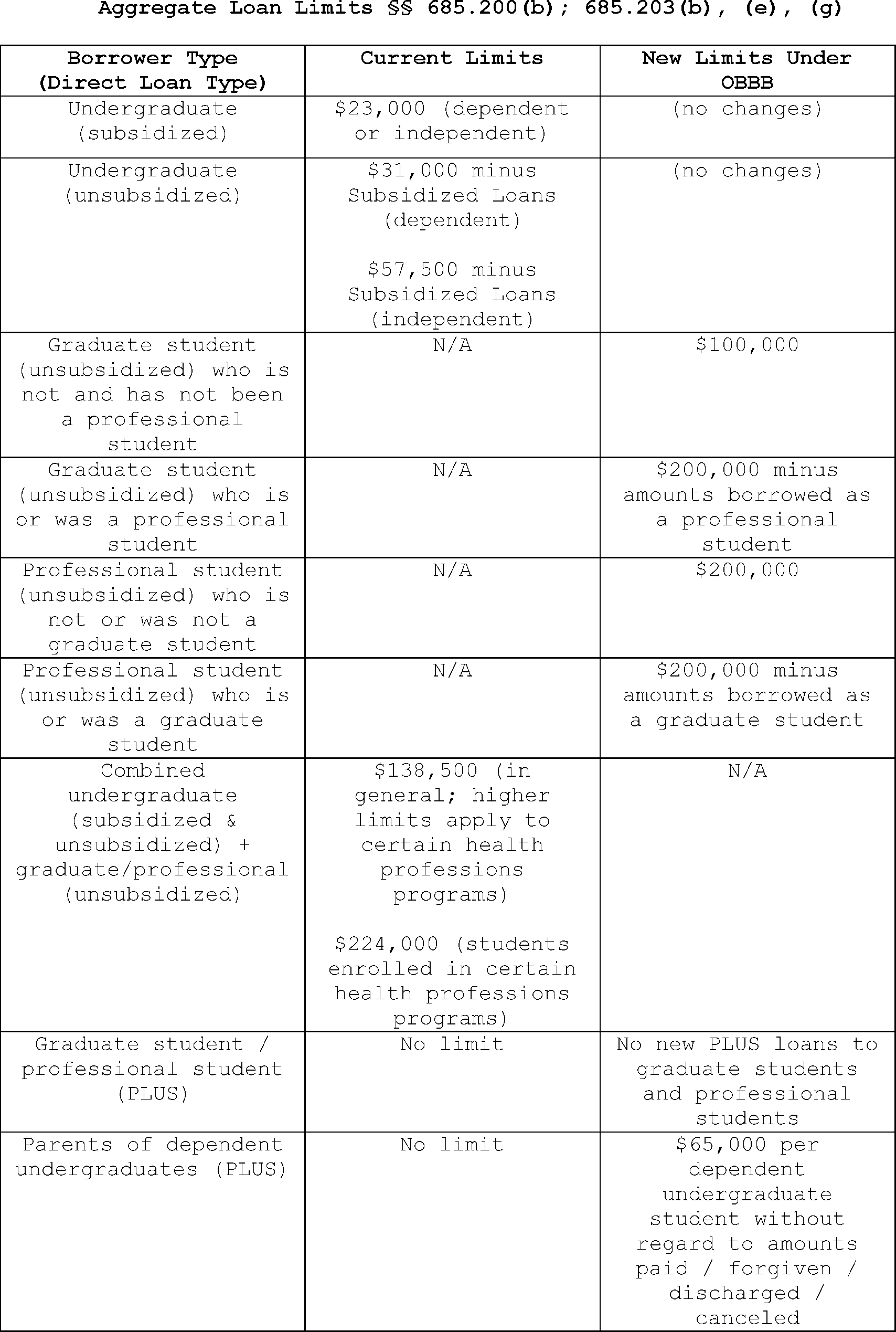

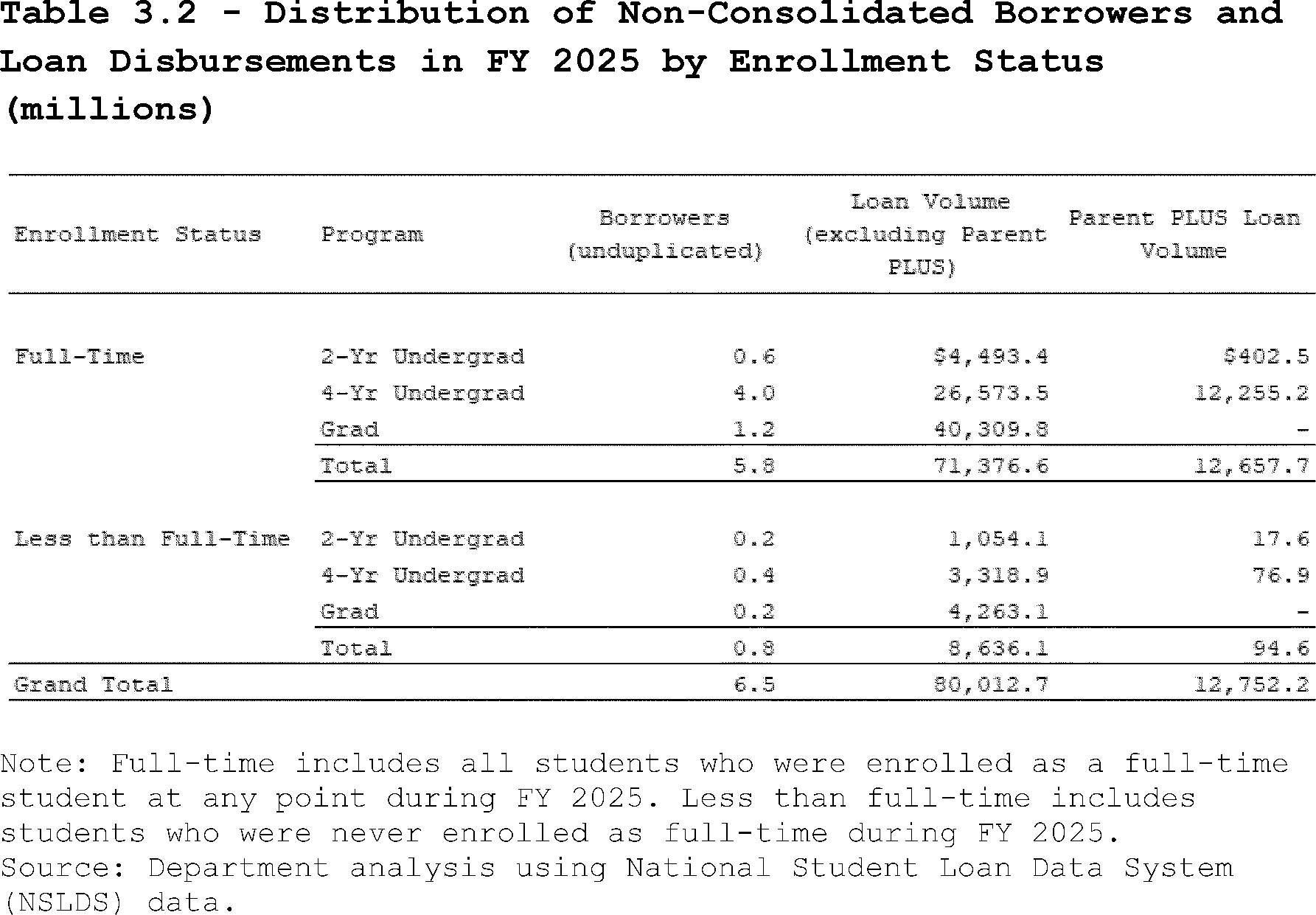

These proposed regulations would reduce outlays received from Direct Loans for institutions of higher education and certain groups of students. There are four main cost areas. First, the OBBB requires institutions to reduce annual loan limits in direct proportion to the percentage of full-time status that the student is enrolled. Prior to the OBBB, part-time students who were enrolled at least half-time could receive the same annual loan amount as students attending full-time. That provision will save taxpayers money by reducing the amounts borrowed by part-time students. Students will also receive less funds as credit balances as a result of the reduced borrowing. Institutions will, as a result, receive less revenue from loans made by the Department on behalf of students. Second, the OBBB limits excessive borrowing by graduate and professional students due to the elimination of unlimited borrowing under the Graduate PLUS Program, maintaining current borrowing limits of $20,500 for graduate students (but limiting borrowing to $100,000 in aggregate), and targeting higher loan limits of $50,000 annually ($200,000 in aggregate) to students enrolled in professional degree programs. Third, the OBBB streamlines the existing myriad of forbearance and deferment options while also limiting the time that borrowers can spend in certain forbearances. These changes should result in more time in active repayment by borrowers, as well as streamlining deferment and forbearance options to the benefit of borrowers, Federal student loan servicers, and taxpayers. Fourth, parents of undergraduate students will also no longer have unlimited borrowing under the Parent PLUS Loan program, which will now be capped at $20,000 per student each year ($65,000 aggregate limit per student). Now parent borrowers, in addition to student borrowers, will have common sense limits on the amount they can borrow to finance their children's postsecondary education.

III. Invitation to Comment

We invite you to submit comments regarding these proposed regulations. Please clearly identify the specific section or sections of the proposed regulations that each of your comments address and arrange your comments in the same order as the proposed regulations. The Department will not accept comments submitted after the comment period closes.

The following tips are meant to help you prepare your comments:

- Please be concise but include objective sources of support for your claims.

- Explain your views as clearly as possible and refrain from using any profanity.

- Refer to specific sections and subsections of the proposed regulations throughout your comments, particularly in any headings that are used to organize your submission.

- Explain why you agree or disagree with the proposed regulatory text and support these reasons with data-driven evidence, including the depth and breadth of your personal or professional experiences. We encourage commenters to include supporting facts, research, and evidence in their comments. When doing so, commenters are encouraged to provide citations to the published materials referenced, including active hyperlinks. Likewise, commenters who reference materials which have not been published are encouraged to upload relevant data collection instruments, data sets, and detailed findings as a part of their comment. Providing such citations and documentation will assist us in analyzing the comments.

- Where you disagree with the proposed regulatory text, suggest alternatives, including regulatory language, and your rationale for the alternative suggestion.

- Do not include PII such as Social Security numbers or loan account numbers for yourself or for others in your submission.

Mass Writing Campaigns: In instances where individual submissions appear to be duplicates or near duplicates of comments prepared as part of a writing campaign, the Department will post one representative sample comment along with the total comment count for that campaign to Regulations.gov. The Department will consider these comments along with all other comments received.

In instances where individual submissions are bundled together (submitted as a single document or packaged together), the Department will post all the substantive comments included in the submissions along with the total comment count for that document or package to Regulations.gov. A well-supported comment is often more informative to the agency than multiple form letters.

Public Comments: The Department invites you to submit comments on all aspects of the proposed regulatory language specified in this Notice of Proposed Rulemaking (NPRM), and in the Regulatory Impact Analysis and Paperwork Reduction Act sections. ( printed page 4256)

The Department may, at its discretion, decide not to post or to withdraw certain comments and other materials that contain promotion of commercial services or products, or are spam.

We may not address comments outside of the scope of these proposed regulations in the final regulations. Comments that are outside of the scope of these proposed regulations are comments that do not discuss the content or impact of the proposed regulations or the Department's evidence or reasons for the proposed regulations.

Comments that are submitted after the comment period closes will not be posted to Regulations.gov or addressed in the final regulations.

We invite you to assist us in complying with the requirements of (E.O.)s 12866 and 13563 and their overall requirement of reducing regulatory burden that might result from these proposed regulations. Please let us know of ways we could reduce potential costs or increase potential benefits while preserving the effective and efficient administration of the Department's programs and activities.

During and after the comment period, you may inspect public comments about these proposed regulations by accessing Regulations.gov.

Assistance to Individuals with Disabilities in Reviewing the Rulemaking Record: On request, we will provide an appropriate accommodation or auxiliary aid to an individual with a disability who needs assistance to review the comments or other documents in the public rulemaking record for these proposed regulations. If you want to schedule an appointment for this type of accommodation or auxiliary aid, please contact the Information Technology Accessibility Program Help Desk at ITAPSupport@ed.gov to help facilitate.

Clarity of the Regulations

Executive Order (E.O.) 12866 and the Presidential memorandum “Plain Language in Government Writing” require each agency to write regulations that are easy to understand. The Secretary invites comments on how to make the regulation easier to understand, including answers to questions such as the following:

- Are the requirements in the proposed regulations clearly stated?

- Do the proposed regulations contain technical terms or other wording that interferes with their clarity?

- Does the format of the proposed regulations (grouping and order of sections, use of headings, paragraphs) aid or reduce its clarity?

- Would the proposed regulations be easier to understand if we divided them into additional (but shorter) sections? (A “section” is preceded by the symbol “§ ” and a numbered heading; for example, § 668.2 General definitions.)

- Could the description of the proposed regulations in theSUPPLEMENTARY INFORMATION section of this preamble be more helpful in making the proposed regulations easier to understand? If so, how?

- What else could we do to make the proposed regulations easier to understand?

- To send any comments that concern how the Department could make these proposed regulations easier to understand, see the instructions in theADDRESSES section.

IV. Background

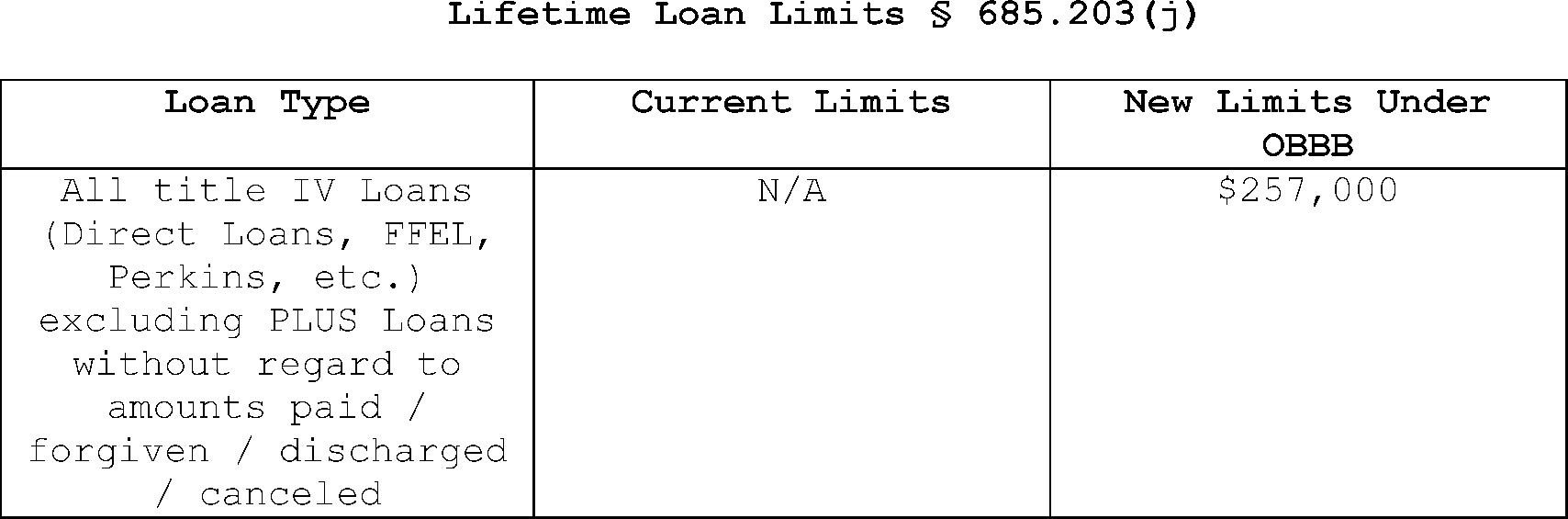

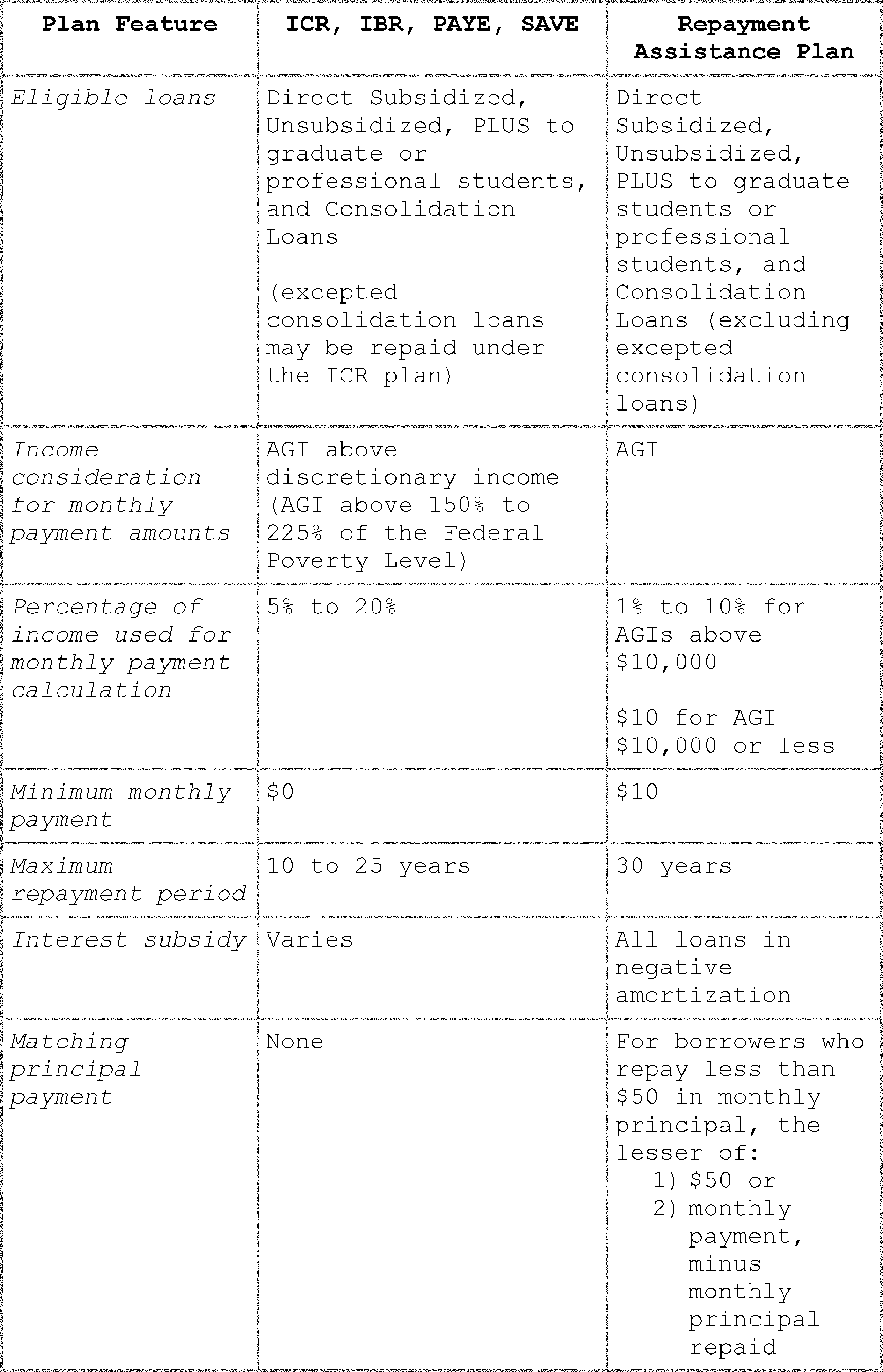

The OBBB, which President Trump signed into law on July 4, 2025, makes extensive statutory changes to fix broken and unnecessarily complex aspects of the Federal student loan programs in the areas of loan limits, repayment plans, and related provisions in title IV. Among other changes, the OBBB sets a new lifetime borrowing cap (approximately $257,500 for most borrowers), eliminates new Graduate PLUS Loans, eliminates unlimited borrowing under the PLUS program for parents, maintains current annual limits under the Direct Loan Program for undergraduate and graduate students, increases annual loan limits for professional degree students, establishes aggregate limits for graduate students, professional degree students, and parents of undergraduates, and reduces annual loan amounts for students enrolled less than full-time. For repayment, the OBBB simplifies and streamlines the current confusing patchwork of repayment plan options for future borrowers to two flexible options: a new Tiered Standard plan for fixed monthly payments over a 10 to 25-year term, and a new income-driven plan called the Repayment Assistance Plan that does not put borrowers deeper in debt by preventing negative amortization over the life of the loan. Confusing, outdated (and in some cases unlawful) repayment plans are phased out, including several existing income-contingent plans, ICR, PAYE, and SAVE (which has been held unlawful in federal court. See Missouri v. Biden, 112 F.4th 531, 538 (8th Cir. 2024)).

This notice of proposed rulemaking complies with Section 492 of the HEA, which requires the Secretary to obtain public input and conduct negotiated rulemaking before issuing proposed regulations for the title IV, HEA programs. To meet those requirements and implement the new statutory directives provided for in the OBBB, the Department convened the Reimagining and Improving Student Education (RISE) negotiated rulemaking Committee. The Committee was composed of representatives of institutions, students and borrowers, State officials, financial aid administrators, loan servicers, and consumer and civil rights organizations. The Committee met over multiple sessions in the fall of 2025 and reached consensus on the entirety of the regulatory text described in this NPRM. In accordance with the protocols established by the Committee, the Department has incorporated the regulatory amendatory text that was mutually agreed upon into this NPRM. Building on the statutory and regulatory history, and the RISE Committee's consensus language, this NPRM conforms Direct Loan rules to the changes enacted in the OBBB by revising loan limit provisions, restructuring repayment options (including IBR and adding the new Repayment Assistance Plan), updating PSLF eligibility and qualifying payment rules, and aligning consolidation, deferment, forbearance, and borrower relief provisions with the new framework.

V. Authority for This Regulatory Action

When Congress passes legislation amending statutory provisions regarding programs administered by an agency, that agency is tasked with implementing those changes in its regulations. The OBBB amended portions of the HEA related to the Federal student loan programs administered by the Department. The Secretary has been granted the broad authority by Congress to implement federal student aid programs under title IV of the HEA, including amendments made by the OBBB. See 20 U.S.C. 1221e-3, see also 20 U.S.C. 1082, 3441, 3474, 3471. In order to carry out functions otherwise vested in the Secretary by law or by delegation of authority pursuant to law, and subject to limitations as may be otherwise imposed by law, the Secretary is authorized to make, promulgate, issue, rescind, and amend rules and regulations governing the manner of operations of, and governing the applicable programs administered by, the Department. See20 U.S.C. 1221e-3. These programs include the Federal student loan programs authorized by the HEA. ( printed page 4257)

Waiver of HEA Master Calendar Requirements

Congress may waive, modify, or rescind requirements in the HEA that require the Department to follow certain processes and procedures when engaging in informal notice-and-comment rulemaking. Specifically, when Congress imposes a statutory deadline that is irreconcilable with other procedural requirements, like in the APA or HEA, then those other procedures have been implicitly waived by Congress. See, e.g., Asiana Airlines v. F.A.A., 134 F.3d 393, 398 (D.C. Cir. 1998); Methodist Hospital of Sacramento v. Shalala, 38 F.3d 1225, 1237 (D.C. Cir. 1998) (finding that certain parts of the APA procedural framework had been waived when Congress gave an agency direction that conflicts with and is irreconcilable with the APA). Indeed, the Harmonious-Reading Canon provides that statutes should be interpretated in a way that renders them compatible, not contradictory. See Scalia & Garner, Reading Law, 180 (2012). As such, the Department does not read statutes to create instructions that directly conflict. Where Congress has given an agency specific direction in a statute that could not be followed if the agency also followed another part of the APA (or HEA, as is relevant here), then the provision is waived.

Here, the OBBB was enacted on July 4, 2025. The OBBB directs the Department to implement roughly a dozen provisions by July 1, 2026. Many of these provisions are not self-executing and could not be implemented absent the Department promulgating regulations to provide details for institutions on how to comply with the OBBB. Congress gave the Secretary discretion within the OBBB to implement the provisions impacting the Federal student loan programs and knew that its commands were not self-executing when directing the Secretary to take action. Congress expected the Secretary to act via rulemaking before July 1, 2026, to enable these provisions to actually go into effect.

The master calendar in the HEA provides that regulatory changes initiated by the Secretary affecting the programs under title IV of the HEA must be published in final form by November 1st in order for them to go into effect by July 1st of the following year. 20 U.S.C. 1089(c)(1). Section 492 of the HEA requires the Department to undertake negotiated rulemaking as part of any regulation under title IV of the HEA. In order to conduct negotiated rulemaking, the Department must have a public hearing (providing notice to the public), solicit nominations from the public to serve on a negotiated rulemaking Committee, select non-Federal negotiators, hold negotiations, develop an NPRM and submit it for review by the Office of Information and Regulatory Affairs (OIRA), publish an NPRM (with at least a 30 day comment period), and then publish a final rule that responds to any substantive comments received. As detailed below, the fastest possible timeframe in which the negotiated rulemaking process for the RISE rulemaking packages could have occurred is 149 days, which is irreconcilable with the timeline allowed by the enactment of the OBBB, due to the fact that there were 120 days between July 4, 2025, (the day the OBBB was enacted), and November 1, 2025, (the publication date of the final rule required by the master calendar).

It would not have been possible for the Department to undertake every step of the negotiated rulemaking process by November 1, 2025, in order to implement the provisions that become effective in the OBBB by July 1, 2026, which is the statutory effective date. Congress was aware of this temporal impossibility when they passed the OBBB, yet Congress decided that these provisions would still go into effect on July 1, 2026. Because these provisions are not self-implementing and cannot go into effect unless the Department promulgates a final rule, the OBBB implicitly waives the master calendar.

For example, Congress directed the Department to publish a schedule of reductions for part-time students to reduce their annual loan eligibility. (Sec. 81001 of the OBBB, P.L. 119-21). The Department announced in DCL: GEN-25-04, published on July 18, 2025, that the schedule of reductions will be issued by the Secretary and used to determine the reduction in the annual loan limits for students who are enrolled less than full-time for subsequent academic years (2026-2027 and beyond). The Department will publish the schedule of reductions in the final rule. This provision was effective upon enactment; however, the 2025-2026 award year had already begun prior to President Trump signing the bill and Federal student loans for that year had already been calculated and initially disbursed. In addition, Congress left open to regulation important details in the Repayment Assistance Program relating to how the Department should treat married borrowers' income, and whether the Department should essentially double count their income when calculating repayment rates. Moreover, in codifying a regulatory definition for professional student that is open-ended, Congress did not fully address what types of programs should be considered professional programs or graduate programs. Indeed, the statute's operative definition of professional degree broadly describes what a professional student is and includes an illustrative list of degrees that meet that operative definition. 34 CFR 668.2 (Noting that the professional degrees “include but are not limited to” the degrees listed). The definition of graduate degree is interrelated to the definition of professional degree, in that a degree is a graduate degree if it awards a graduate credential but is not a professional degree.

With these important details unanswered by the plain text of the OBBB, it is clear that the policy scheme set forth in the HEA made by the OBBB cannot be implemented absent regulatory action by the Department.

At the same time, even though the requirements of negotiated rulemaking are onerous, it is possible to undergo negotiated rulemaking and publish a final rule at least 30 days prior to the effective date of these OBBB provisions on July 1, 2026. Therefore, the OBBB does not waive negotiated rulemaking nor any provision in the APA. For provisions in the OBBB that become effective July 1, 2027, and beyond, Congress did not implicitly repeal the master calendar because it is possible for the Department to publish a final rule that complies with the master calendar to implement those provisions. Nonetheless, the Department is conducting rulemaking relating to those provisions that go into effect in 2027 and beyond due to the interconnected nature of these provisions as they relate to Federal student aid programs.

VI. Public Participation

Section 492 of the HEA, 20 U.S.C. 1098a, requires the Secretary to obtain public involvement in the development of proposed regulations affecting the title IV, HEA programs. Prior to developing this NPRM, the Department obtained advice and recommendations from individuals and representatives of groups involved in the title IV, HEA programs. This outreach included a 30-day public comment period, one day of public hearings, and culminated in nine days of in-person negotiated rulemaking at the Department's headquarters in Washington, DC. Further details regarding these efforts are provided below.

On July 25, 2025, the Department published in the Federal Register (90 ( printed page 4258) FR 35261) a notice of our intent to hold a public hearing and to establish two negotiated rulemaking Committees to consider regulatory changes to the title IV, HEA programs included in the OBBB with one Committee focusing on topics regarding annual and aggregate loan limits, loan deferment, forbearance, and repayment, among others, related to Federal student loans.

Public Comments and Hearings

We received 1,864 written comments in response to the Federal Register notice. Additionally, we held a virtual public hearing on August 7, 2025. A total of 57 individuals testified virtually at the hearing.

You may view the written comments submitted in response to the July 29, 2025 “Intent to Establish Negotiated Rulemaking Committees; Correction” correction notice (90 FR 35652), by visiting the Federal eRulemaking Portal at Regulations.gov, within docket ID ED-2025-OPE-0151. Instructions for finding comments are also available on the site under “FAQ.”

Transcripts of the public hearings can be accessed at https://www.ed.gov/laws-and-policy/higher-education-laws-and-policy/higher-education-policy/negotiated-rulemaking-for-higher-education-2025-2026.

Negotiated Rulemaking

On July 25, 2025, we published a notice in the Federal Register announcing our intent to establish one Committee to prepare these proposed regulations (90 FR 35261). The notice set forth a schedule for Committee meetings and requested nominations for individual, non-Federal negotiators to serve on the negotiated rulemaking Committee. In the notice, we also announced the topics that the Committee would address.

We chose members of the negotiated rulemaking Committee from individuals nominated by groups involved in the title IV, HEA programs. We selected individuals with demonstrated expertise or experience with the student loan program. The negotiated rulemaking Committee included the following members, representing their respective constituencies:

- Legal assistance organizations that represent students and borrowers, consumer advocates, and civil rights groups that represent students: Ashley Naporlee, Lead Attorney, Consumer Protection Team, Legal Aid Society of San Diego, and Tamar Hoffman (alternate), Staff Attorney, Homeownership and Consumer Rights Unit, Community Legal Services of Philadelphia.

- Student loan servicers, collection agencies, lenders, and guaranty agencies: Alexander Ricci, President, National Council of Higher Education Resources, and Lori Hartung (alternate), Regional Sales Executive, Education Computer Systems, Inc.

- Organizations representing taxpayers and the public interest: Alexander Holt, Senior Advisor on Higher Education, Committee for a Responsible Federal Budget, and Dr. Andrew Gillen (alternate), Research Fellow, Cato Institute.

- Private nonprofit institutions of higher education including institutions eligible to receive Federal assistance under Title III and Title V of the HEA tribal colleges and universities, and historically black colleges and universities: Jenna Colvin, President, Georgia Independent College Association, and Patti Kohler (alternate), Vice President of Financial Aid, Western Governors University.

- Proprietary institutions of higher education, as defined in34 CFR 600.5: Dr. Andy Vaughn, President and Chief Executive Officer, Alliant International University, and Jeffrey Bodimer (alternate), Vice President of Regulatory Compliance and Financial Aid, Post University.

- Public institutions of higher education including institutions eligible to receive Federal assistance under Title III and Title V of the HEA, tribal colleges and universities, and historically black colleges and universities: Dr. Timothy B. King, Vice Provost for Student Success, Jacksonville State University, and Matthew Ellsworth (alternate), Director of Financial Aid, Western Carolina University.

- State officials, including State student grant agencies, State higher education executive officers, and representatives of authorizing agencies: Scott Kemp, Student Loan Advocate, State Council of Higher Education for Virginia, and Dr. Bennett Boggs (alternate), Commissioner, Missouri Department of Higher Education & Workforce Development.

- Student loan borrowers, including borrowers in school, deferment, forbearance, delinquent, default, and currently in repayment: Deborah Lilly, Senior Project Manager, UnitedHealthcare, and Emeka Oguh (alternate), Chief Executive Officer, PeopleJoy.

- Student loan borrowers who are veterans, U.S. military service members, or groups representing them: Faisal Sulman, Legal Fellow, Student Veterans of America, and Robert H. Carey, Jr. (alternate), Executive Director, National Defense Committee.

The Committee discussion was led by Tamy Abernathy, Director of the Policy Coordination Group of the Department and supported by the Department's Office of General Counsel and Office of Postsecondary Education, with Annmarie Weisman of Federal Student Aid serving as facilitator for the Committee.

The negotiated rulemaking Committee for these proposed regulations met from September 29 to October 3, 2025, and November 3 to November 6, 2025, which concluded the negotiations on November 7, 2025, a day earlier than originally scheduled. The Committee reviewed and discussed draft regulations prepared by the Department, as well as alternative regulatory language and suggestions proposed by Committee members. Additionally, during each negotiated rulemaking meeting, some non-Federal negotiators shared feedback that they had received from stakeholders in their respective constituencies. This approach facilitated the inclusion of a wide array of ideas and perspectives, which contributed to the development of the consensus language.

Under the organizational protocols for negotiated rulemaking agreed to by all members of the Committee, if the Committee reaches consensus on the proposed regulations, the Department agrees to publish, without substantive alteration, a defined group of regulations on which the Committee reached consensus—unless the Secretary reopens the process or provides a written explanation to the participants stating why she has decided to depart from the agreement reached during negotiations. In this instance, consensus is considered to be the absence of dissent by any member of the negotiated rulemaking Committee (abstaining members are not considered to be dissenting from the proposal). The Committee reached consensus on the entirety of the draft regulations on November 6, 2025. As a result, this NPRM reflects the consensus language without any substantive changes.

Further information on the negotiated rulemaking process can be found at: https://www.ed.gov/laws-and-policy/higher-education-laws-and-policy/higher-education-policy/negotiated-rulemaking-for-higher-education-2025-2026.

VI. Significant Proposed Regulations

We discuss substantive issues under the sections of the proposed regulations to which they pertain. While we generally do not address technical, ( printed page 4259) minor, or legal changes to the proposed amendatory text, there are a few areas where we determined technical corrections were necessary and we fully explain those later in the sections where the corrections have been made in this NPRM.

Federal Perkins Loan Program

Loan Rehabilitation (§ 674.39)

Statute: Section 82003(a)(2) of the OBBB amends

Section 464(h)(1)(D) of the HEA to provide that loan rehabilitation for defaulted Federal Perkins loans is limited to a maximum of two times per loan. Section 82003(a)(3) of the OBBB provides that the effective date of this statutory change is July 1, 2027.

Current Regulations: Section 674.39 contains the general terms and conditions pertaining to loan rehabilitation in the Federal Perkins Loan Program. Specifically, § 674.39(e) provides that a borrower may rehabilitate a defaulted Federal Perkins Loan only one time.

Proposed Regulations: The Department proposes to amend the regulations in § 674.39(e) to provide that on or after July 1, 2027, a borrower may rehabilitate a defaulted loan a maximum of two times. This means that a borrower who has previously rehabilitated a defaulted loan but who has subsequently defaulted may begin the process of rehabilitating a loan on or after July 1, 2027, to bring their loan back into good standing and resume repayment.

Reasons: The proposed regulations reflect the changes made by Section 82003(a)(2) of the OBBB, which amended Section 464(h)(1)(D) of the HEA to update the loan rehabilitation limits for the Federal Perkins Loan Program. Additionally, Section 82003(a)(3) of the OBBB provides that the effective date of this statutory change takes effect beginning on July 1, 2027. Because borrowers with outstanding Federal Perkins Loans would now have the ability to rehabilitate a defaulted loan a maximum of two times beginning July 1, 2027, we believe that the regulations should reflect the number of times a borrower may rehabilitate this type of loan before and after July 1, 2027.

Accordingly, the Department proposes to bifurcate the limitations on loan rehabilitations for the Federal Perkins Loan Program: proposed § 674.39(e)(1) would retain the limitation in the current regulations that would be in effect prior to July 1, 2027, whereby a borrower can only obtain the benefit of loan rehabilitation once for a defaulted Federal Perkins Loan. Proposed § 674.39(e)(2) would provide that on or after July 1, 2027, a borrower may rehabilitate a defaulted Federal Perkins Loan a maximum of two times. This bifurcation would make clear the number of times a borrower may rehabilitate based on the date of rehabilitation.

During the negotiated rulemaking sessions, non-Federal negotiators focused on how the Department should treat traditional loan rehabilitations completed during the COVID-19 payment pause, particularly for purposes of the statutory limit on the number of rehabilitations available to a borrower. Negotiators emphasized that some borrowers completed “real” rehabilitations during the pause—often in circumstances where Fresh Start later became available—and urged the Department to make certain that those COVID-period rehabilitations would not count against the borrower's total number of rehabilitation attempts, given the unusual operational environment and the availability of alternative default-resolution pathways during the pandemic. We explained that, while Fresh Start [1] is a distinct initiative and does not constitute rehabilitation, a borrower who completed a rehabilitation during the payment pause, is considered to have completed the rehabilitation process once. During this time, borrowers were only permitted to rehabilitate their loans one time under the statute. Therefore, because those borrowers completed rehabilitation in accordance with statutory requirements, the Department does not have the authority to disregard the rehabilitation when applying the statutory maximum. However, under the OBBB, effective July 1, 2027, the statute has increased the limit of rehabilitations to twice.

Federal Family Education Loan (FFEL) Program

Loan Rehabilitation Agreement (§ 682.405)

Statute: Section 82003(a)(1) of the OBBB amends section 428F(a)(5) of the HEA to change the loan rehabilitation limit in that section to reflect that a defaulted loan may be rehabilitated twice. Prior to the OBBB, such loans could only be rehabilitated once. Section 82003(a)(3) of the OBBB provides that the effective date of this statutory change is July 1, 2027.

Current Regulations: Section 682.405 contains the general terms and conditions of rehabilitation of defaulted loans made through the Federal Family Education Loan (FFEL) program, which are administered by a guaranty agency. Section 682.405(a)(3) provides that if a borrower's FFEL program loan is being collected through administrative wage garnishment (AWG) while the borrower is also rehabilitating that loan under a rehabilitation agreement, the guaranty agency must continue AWG until the borrower makes five qualifying monthly payments under such rehabilitation agreement. After receiving the fifth monthly payment, the guaranty agency suspends the AWG order. Such a borrower may only obtain the benefit of a suspension of AWG while also attempting to rehabilitate a defaulted FFEL program loan once. Section 682.405(a)(4) provides that after the FFEL program loan has been rehabilitated, the borrower regains eligibility and the benefits afforded to non-defaulted borrowers, including access to certain deferments, from the date of the rehabilitation. Section 682.405(a)(4) further provides that for any loan that is rehabilitated on or after August 14, 2008, the borrower cannot rehabilitate the loan again if the loan returns to default status following the rehabilitation.

Proposed Regulations: The Department proposes to amend the regulations at § 682.405(a)(3)(iii)(B) to provide that on or after July 1, 2027, a borrower may only obtain the suspension of AWG benefit one time per each attempt to rehabilitate a defaulted loan. Furthermore, the Department also proposes that a loan may only be rehabilitated once between August 14, 2008, through June 30, 2027. On or after July 1, 2027, a loan may be rehabilitated a maximum of two times over the loan's lifetime, regardless of when the loan was made.

Reasons: The regulations are amended to reflect the changes made by the OBBB. The Department also amends proposed § 682.405(a)(3)(iii) to correct an administrative error that includes adding paragraph (A) and (B). This proposed additional language is needed to distinguish the number of times a FFEL borrower may rehabilitate their defaulted loans before and after June 30, 2027, and its impact on the suspension of AWG. Accordingly, we revised current § 682.405(a)(3)(iii) to proposed § 682.405(a)(3)(iii)(A), which would only apply for loans on or before June 30, 2027, and state that a borrower may only obtain the benefit of a suspension of AWG while also attempting to rehabilitate a defaulted loan once. ( printed page 4260) Proposed § 682.405(a)(3)(iii)(B) would apply to loans obtained on or after July 1, 2027, and states that a borrower may only obtain the suspension of AWG benefit one time per each attempt to rehabilitate a defaulted loan. We believe separating these provisions at the subparagraph level would make clear that suspension of AWG remains available for one eligible rehabilitation through June 30, 2027, and provides that the suspension would be available for up to a maximum two rehabilitations per loan on or after July 1, 2027.

Income-Based Repayment Plan (§ 682.215)

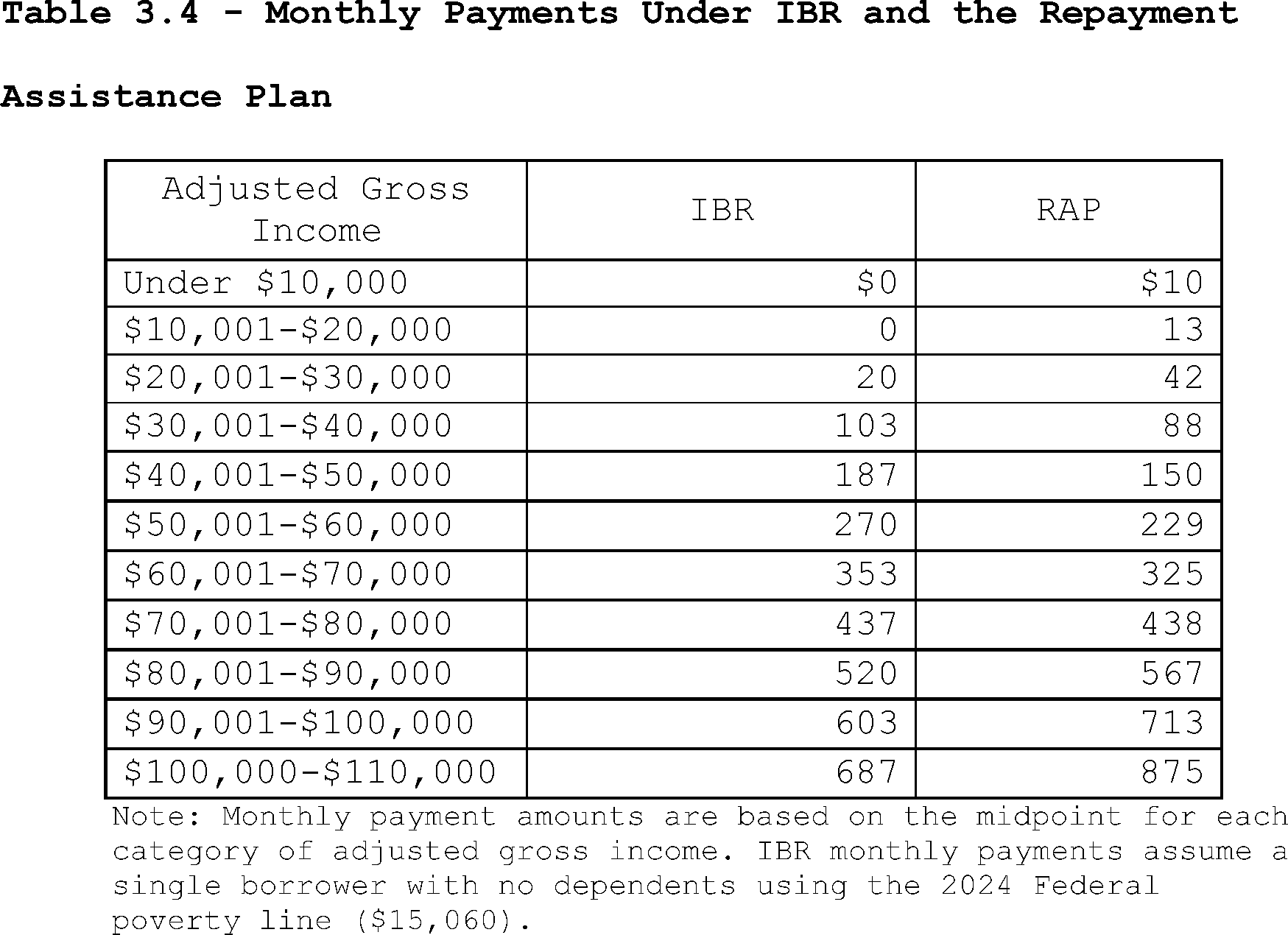

Statute: Section 82001(f)(1)(B) of the OBBB amends Section 493C(a)(3) of the HEA to eliminate the requirement that FFEL borrowers must have a partial financial hardship to be eligible for IBR. Section 82001(g) of the OBBB amends Section 428(b)(9)(A)(v) of the HEA to remove the partial financial hardship requirement from IBR for FFEL Loans. The OBBB also creates the definition of applicable amount in Section 493C(a)(3) of the HEA. These provisions were effective upon enactment, and the Department has already taken steps to eliminate the requirement that borrowers show a partial financial hardship to participate in existing IDR plans.

Current Regulations: Section 682.215 contains the regulations on the IBR plan for FFEL program loans. Section 682.215(a) provides the definitional terms that are applicable to the IBR plan, including a definition of partial financial hardship. Section 682.215(b) provides the terms and conditions of the IBR plan, including a borrower's eligibility for the IBR plan and the calculation of a borrower's monthly payment under the plan. In current regulations, to enroll in the IBR plan, the borrower must have a partial financial hardship and the borrower's monthly loan payments are limited to no more than 15 percent of the amount by which the borrower's adjusted gross income exceeds 150 percent of the poverty line income applicable to the borrower's family size, divided by 12.

Section 682.215(d) provides for changes in a borrower's payment amount if a borrower no longer has a partial financial hardship or if a borrower elects to repay their loans under a different repayment plan. Section 682.215(e) provides the eligibility documentation, verification, and notification requirements to determine a borrower's initial or continued eligibility for the IBR plan or to calculate a monthly payment under such plan. Finally, Section 682.215(f) provides the loan forgiveness provisions under the IBR plan: in general, a borrower receives forgiveness of the remaining balance of their loans after the borrower has made 300 qualifying monthly payments (or 25 years) under IBR.

Proposed Regulations: To conform the regulations to changes of the HEA that were enacted by the OBBB, we are proposing to amend the regulations at § 682.215(a)(4) to remove the definition of partial financial hardship and include a new definition of applicable amount. Applicable amount would mean for the purposes of the IBR plan, 15 percent of the result obtained by calculating, on at least an annual basis, the amount by which the adjusted gross income of the borrower and the borrower's spouse (if applicable) exceeds 150 percent of the poverty guideline. We also propose to amend the terms and conditions of the IBR plan in § 682.215(b), including a borrower's eligibility for the IBR plan and the calculation of a borrower's monthly payment under the IBR plan by removing references to partial financial hardship, and where appropriate, replacing references to partial financial hardship with a provision of the applicable amount calculated under IBR. Finally, we propose to amend the forgiveness provisions in IBR plan in § 682.215(f) by removing references to partial financial hardship.

Reasons: The regulations are amended to reflect the changes made by the OBBB, including the definition of applicable amount. The term applicable amount by and large supplants partial financial hardship, and we propose making conforming changes throughout § 682.215 by removing partial financial hardship or removing the concepts of partial financial hardship by using applicable amount instead. Additionally, the Department removed the definition of partial financial hardship in § 682.215(a)(4) and removed the term throughout the section.

William D. Ford Federal Direct Student Loan (Direct Loan) Program

Definitions (§ 685.102)

Statute: Section 81001(2) of the OBBB amends Section 455(a) of the HEA and defines the following terms: expected time to credential, graduate student,professional student, and program length.

Current Regulations: Section 685.102 contains the definitions that apply to 34 CFR part 685. Specifically, § 685.102(a)(1) provides a list of common definitions for all the title IV, HEA programs in 34 CFR part 668 (Student Assistance General Provisions) that also apply to 34 CFR part 685.

Proposed Regulations: To implement the new provisions enacted in the OBBB, we propose to add several new definitions for the purposes of the Direct Loan Program. We propose to add in § 685.102(b) the following new definitions: expected time to credential; graduate student;professional student; and program length.

We propose to define expected time to credential to mean the expected time for a student to complete a program that is the lesser of (1) three academic years or (2) the period determined by calculating the difference between the length of the academic program and the period the student already completed in that academic program.

We propose to define graduate student to mean a student who is enrolled in a program of study that is above the baccalaureate level and awards a graduate credential (other than a professional degree) upon completion of the program. Above the baccalaureate level means that the program ordinarily requires, as a prerequisite for enrollment, that a student first obtain a baccalaureate degree. For the purposes of dual degree programs that allow individuals to complete a bachelor's degree and either a graduate or professional degree within the same program, a student is considered an undergraduate student for at least the first three years of that program. 34 CFR 668.2(b).

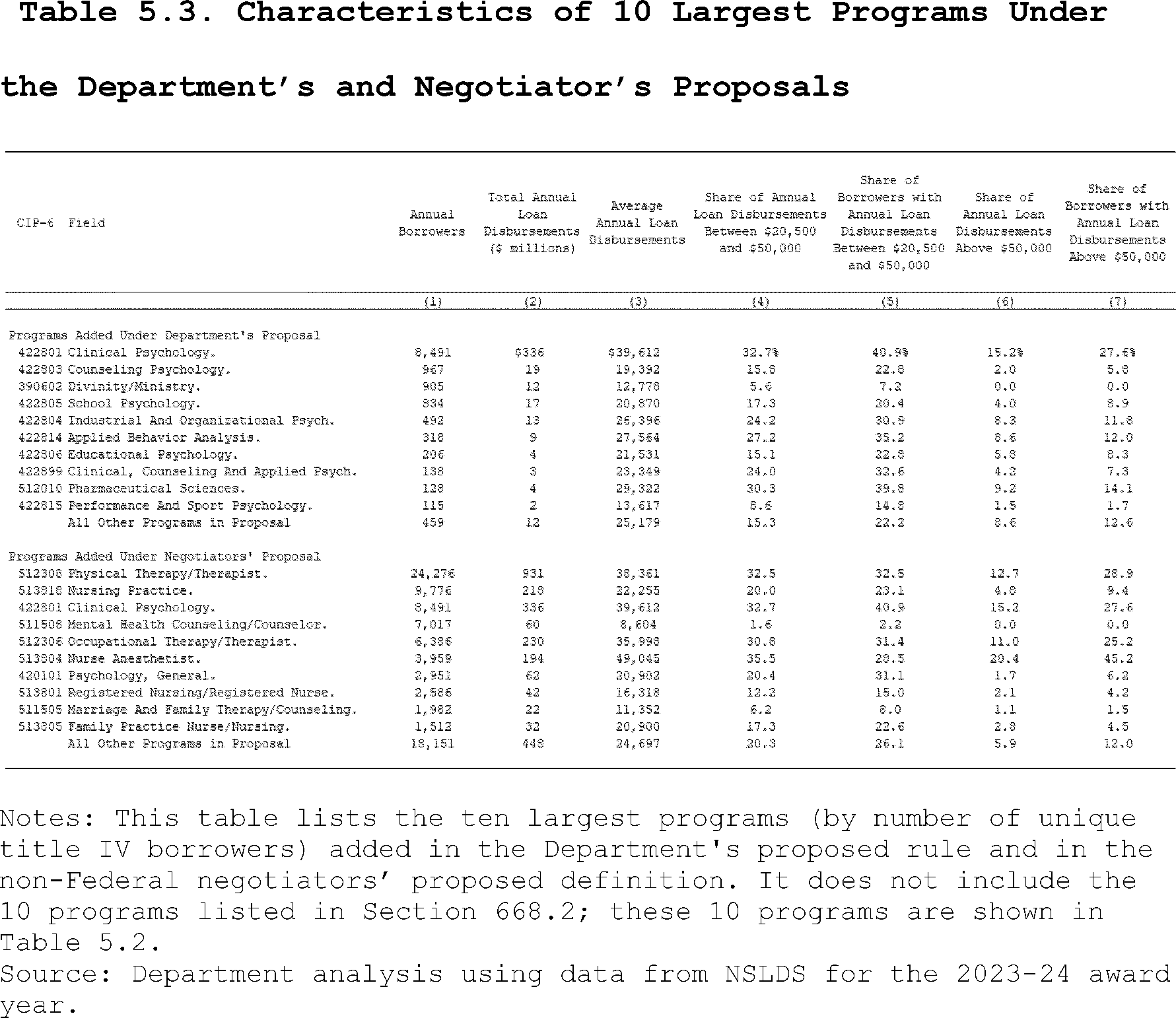

We propose to define professional student to mean a student enrolled in a program of study that awards a professional degree upon completion of the program. In defining professional student, we apply the definition of a professional degree in 34 CFR 668.2 that was in effect on July 4, 2025, and clarify that such degrees meet the following elements: signifies both completion of the academic requirements for beginning practice in a given profession and a level of professional skill beyond that which is normally required for a bachelor's degree; is generally at the doctoral level; requires at least six academic years of postsecondary education coursework for completion, including at least two years of post-baccalaureate level coursework; generally requires professional licensure to begin practice; and, includes a four-digit program Classification of Instructional Program (CIP) code, as assigned by the institution or determined by the Secretary, in the same intermediate group in certain fields. We also propose that a professional degree only includes ( printed page 4261) degrees in the following fields: [2] Pharmacy (Pharm.D.), Dentistry (D.D.S. or D.M.D.), Veterinary Medicine (D.V.M.), Chiropractic (D.C. or D.C.M.), Law (L.L.B. or J.D.), Medicine (M.D.), Optometry (O.D.), Osteopathic Medicine (D.O.), Podiatry (D.P.M., D.P., or Pod.D.), Theology (M.Div., or M.H.L.), and Clinical Psychology (Psy.D. or Ph.D.). Finally, we propose that a professional student may not receive title IV aid as an undergraduate student for the same period of enrollment and must be enrolled in a program leading to a professional degree. The Department seeks comment on its analysis relating to the professional degrees it included in or excluded from the professional student definition. Specifically, it would be useful to have feedback on how the Department applied the operative definition of professional student and utilized the context of the illustrative list of degrees when interpreting the definition.

We propose to define program length to mean the minimum amount of time in weeks, months, or years that is specified in the catalog, marketing materials, or other official publications of an institution for a full-time student to complete the requirements for a specific program of study.

Reasons: In the definition of expected time to credential (implementing Section 455(a)(8)(B) of the HEA, added Section 81001 of the OBBB), we begin the definition with “From July 1, 2026.” Section 455(a)(3)(C), (4), (5), and (6) of the HEA, added by Section 81001 of the OBBB, terminates the Department's authority to make Federal Direct PLUS Loans to graduate and professional students, imposes new annual and aggregate limits for Federal Direct Unsubsidized Loans made to graduate and professional students, and imposes new annual and aggregate limits for Federal Direct PLUS Loans. Each of these statutory provisions takes effect on July 1, 2026. Therefore, the definition of expected time to credential, begins with “July 1, 2026” because the term is used in regard to the limited exception to Sections 455(a)(3)(C), (4), (5), and (6) of the HEA, added by Section 81001 of the OBBB, for currently enrolled students.

Additionally, in paragraph (1) of the definition of expected time to credential, we propose adding a cross reference to the definition of the term academic year in 34 CFR 668.3. Because this definition applies to loan limits, we believe using this cross reference to academic year, as defined in § 668.3, would be consistent with existing policy such as that reflected in § 685.203(h), where the loan limit period applies to an academic year as defined in 34 CFR 668.3.

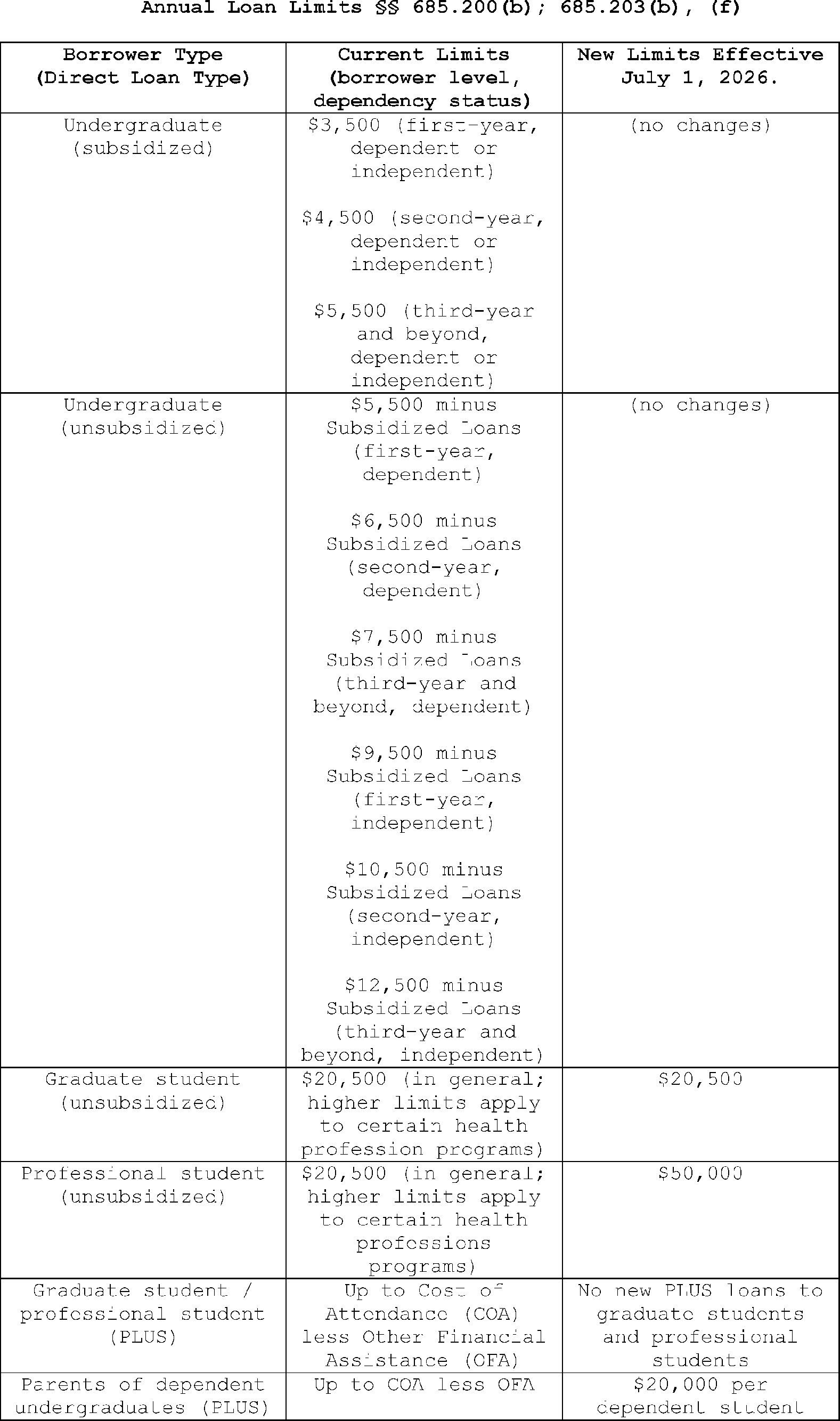

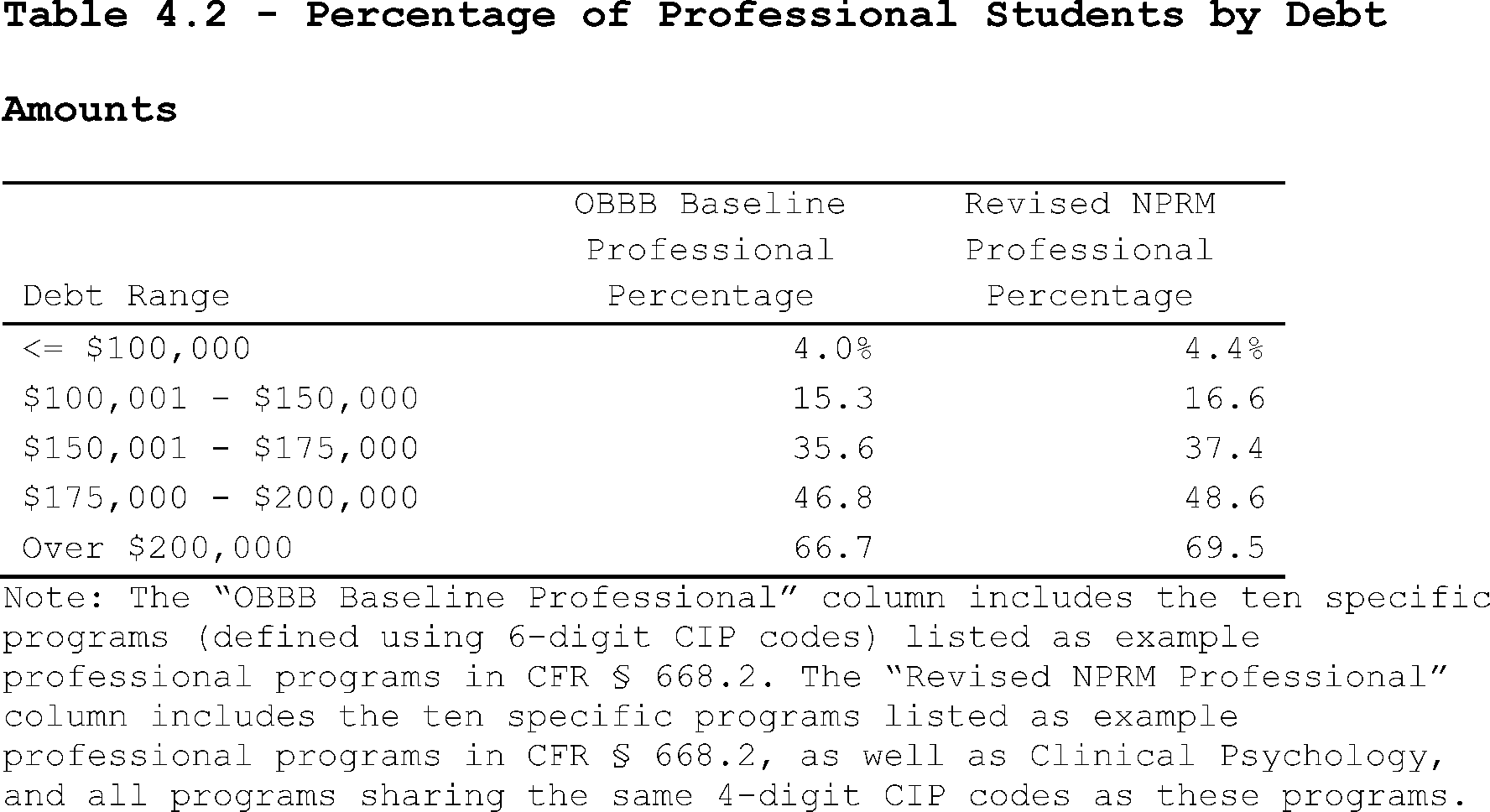

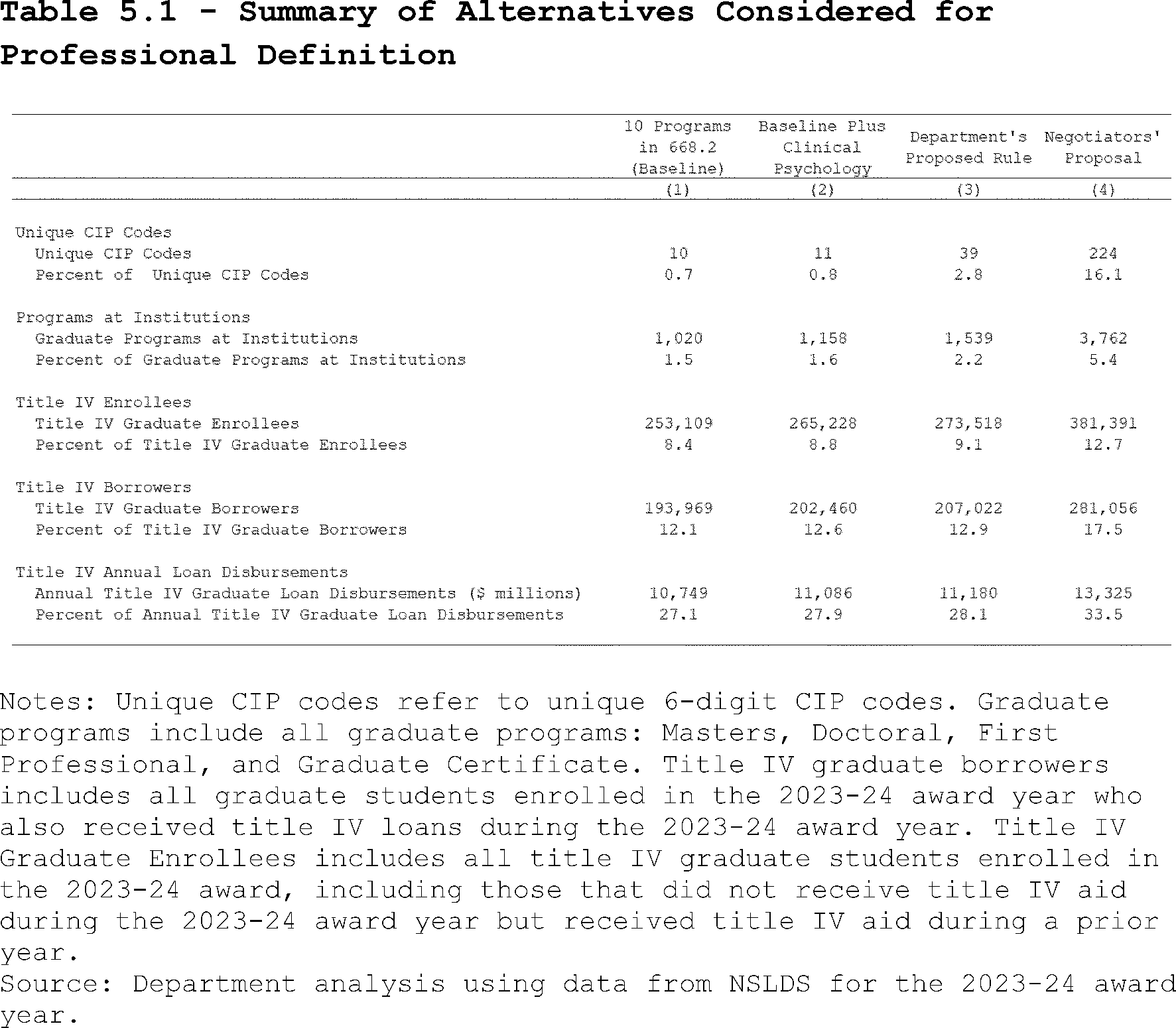

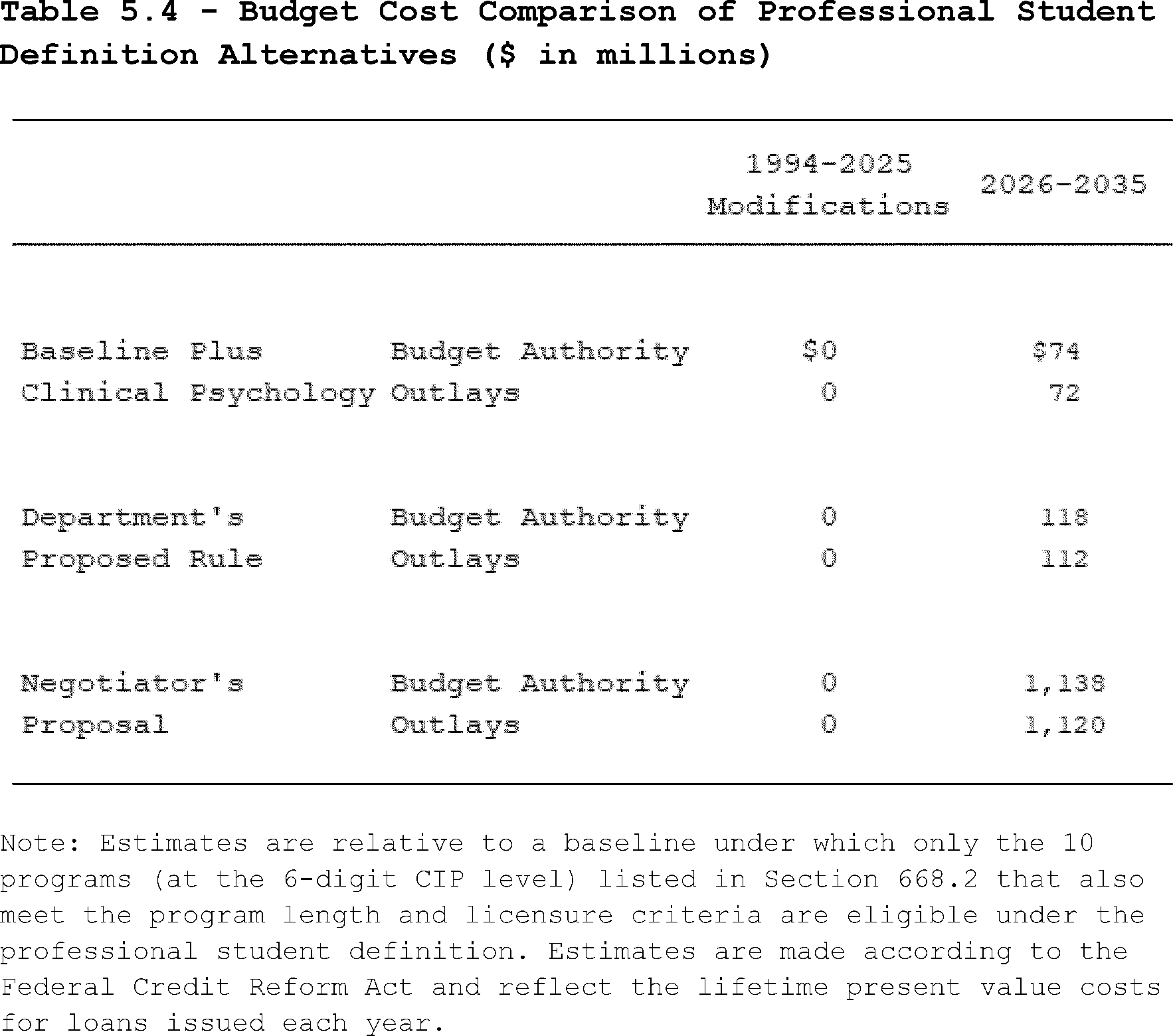

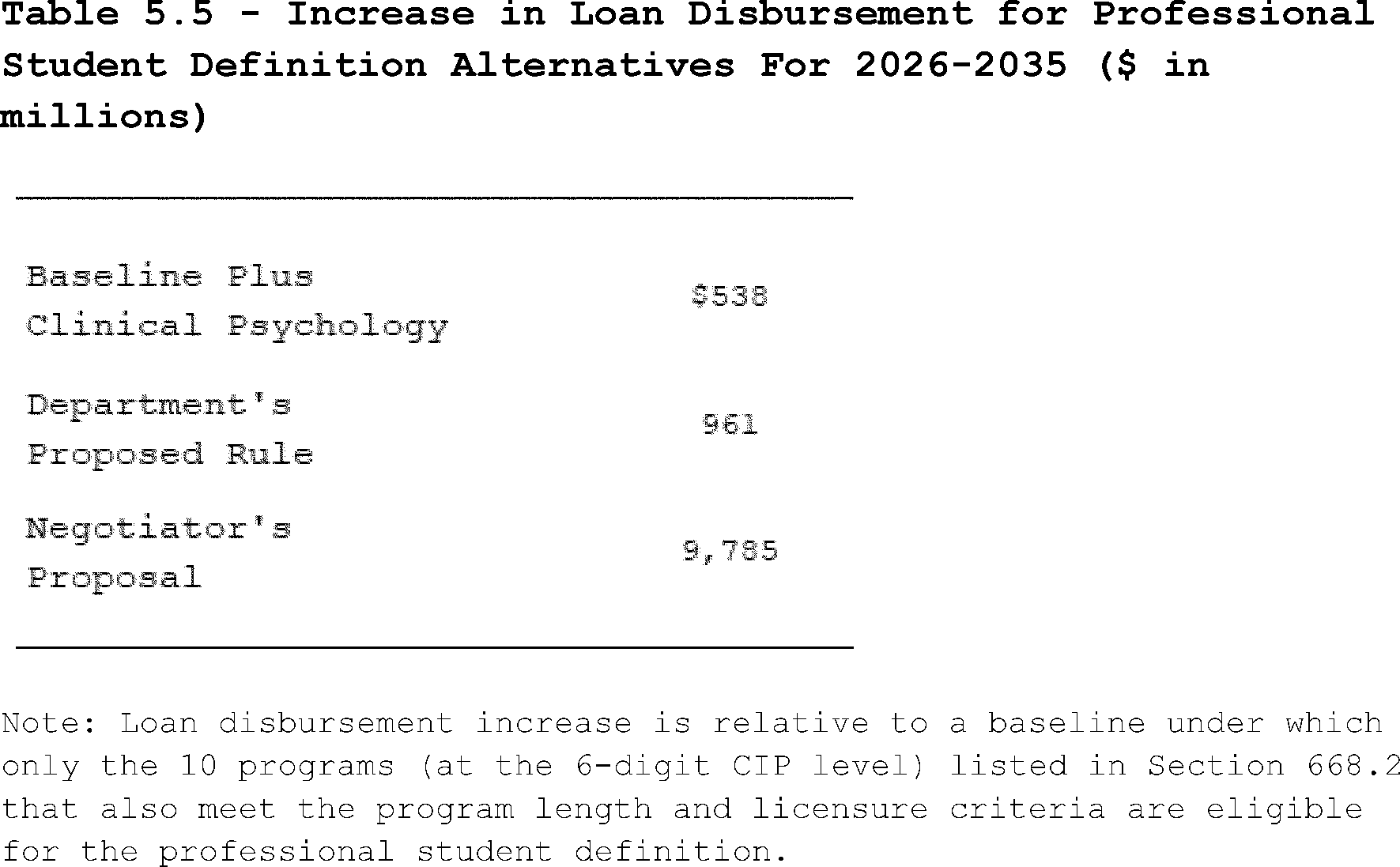

Changes enacted in the OBBB, effective for loans made on or after July 1, 2026, limit borrowing amounts for graduate students to an annual limit of $20,500, with an aggregate lifetime limit of $100,000. For those students enrolled in professional degree programs, the annual limit is $50,000, with an aggregate lifetime limit of $200,000.

Due to the significant difference between the loan limits for graduate students compared to the limits for students enrolled in professional degree programs, institutions, relevant trade associations, and other stakeholders have been seeking to have graduate degree programs that have historically not been identified as first professional or professional degree programs to be classified as such, since the OBBB was signed into law.[3] Labeling such programs as professional degrees would significantly increase the amount of Federal student loans that a borrower may have access to more than doubling the annual loan limit and doubling the lifetime access for graduate students.

In the definition of graduate student ( see Section 455(a)(4)(C)(i) of the HEA), we include the clause that a graduate student is a “student enrolled in a program of study that is above the baccalaureate level” to make clear that the academic program needs to be above the baccalaureate level to be considered eligible for the higher graduate student loan limits. This proposed change incorporates the current definition of graduate or professional student in § 668.2 and a long-standing policy for the Federal Pell Grant, Federal Supplemental Opportunity Grant (FSEOG), and student loan programs that a graduate student is a student who is enrolled in a program or course above the baccalaureate level. Words and phrases typically carry their ordinary and everyday meaning. Scalia & Garner, Reading Law: The Interpretation of Legal Texts, 69 (2012). The term “graduate” in this context ordinarily means an advanced college degree program that requires, as a condition of enrollment, that a student must have graduated from a lower-level postsecondary program (otherwise known as an “undergraduate degree”). The common understanding of the nomenclature “graduate” in this context has always implicitly referred to individuals who have graduated from a baccalaureate degree program, as opposed to graduates of certificate degree or associate's degree programs.[4] Both baccalaureate degrees and associate's degrees are undergraduate degrees, but an associate's degree is not sufficient for a student to enroll in a graduate degree program. Here, we provide that a graduate student must be a student enrolled in a program above the baccalaureate level.

For the purpose of the Direct Loan limits established in section 81001 of the OBBB, Congress made it clear that “ a graduate student, who is not a professional student,” will continue to receive the current loan limit of $20,500 for unsubsidized loans after July 1, 2026. 20 U.S.C. 1087e(a)(4)(A)(i). The OBBB made no change in the annual loan limit for Direct Unsubsidized Loans for which graduate students can qualify.

To distinguish between graduate students and professional students, Section 81001 of the OBBB amends Section 455(a) of the HEA by defining a professional student to mean “a student who is enrolled in a program of study that awards a professional degree (as that term is defined under section 668.2 of title 34, Code of Federal Regulations, and in effect on the date of enactment of July 4, 2025), upon completion of the program.” The OBBB defines graduate student as “a student ( printed page 4262) enrolled in a program of study that awards a graduate credential (other than a professional degree) upon completion of the program.”

The definition of professional degree in 34 CFR 668.2 that is referenced in 20 U.S.C. 1087e(a)(4)(C)(ii) and was in effect on the OBBB date of enactment of July 4, 2025, reads as follows:

Professional degree: A degree that signifies both completion of the academic requirements for beginning practice in a given profession and a level of professional skill beyond that normally required for a bachelor's degree. Professional licensure is also generally required. Examples of a professional degree include but are not limited to Pharmacy (Pharm.D.), Dentistry (D.D.S. or D.M.D.), Veterinary Medicine (D.V.M.), Chiropractic (D.C. or D.C.M.), Law (L.L.B. or J.D.), Medicine (M.D.), Optometry (O.D.), Osteopathic Medicine (D.O.), Podiatry (D.P.M., D.P., or Pod.D.), and Theology (M.Div., or M.H.L.).

In applying this long-standing definition to the new loan limits for graduate and professional students, the inclusion of the phrase in the definition that “[e]xamples of a professional degree include but are not limited to . . .” suggests that the list of examples provided in the definition need not be exhaustive. Conversely, the list is not completely open-ended, as it provides an illustrative list and a three-part test to draw upon.

Rather than constructing a definition for professional student, Congress borrowed and codified the Department's regulatory definition of the term “professional degree” in 34 CFR 668.2. This definition served a very limited purpose in the Department's regulations, and the Department has not identified any interest in the prior use of the term “professional degree” that will be impaired by its adoption below. However, the Department seeks public feedback on whether any pre-existing interest in the regulation will be affected.

In adopting this definition of “professional degree,” Congress incorporated a variety of words and phrases that may, without context, appear ambiguous or vague on their face or as applied to specific degree programs. The Department must identify the best reading of the statute using the tools of statutory construction.

The operative definition provided in the OBBB establishes a three-part test: First, the degree must signify completion of the academic requirements for beginning practice in a given profession. The word “signify” means to be a sign of something ( https://www.merriam-webster.com/dictionary/signify). Here, it means when the degree is completed, the recipient has completed all academic requirements to begin practicing in a profession, even if some additional training is required.

Second, the profession the graduate enters must require a level of professional skill beyond what is normally required for a bachelor's degree. This means that the profession must require skill(s) that students who only have a bachelor's degree (or training below a bachelor's degree level) would not normally have. The term “normally” connotes that this rule will be followed in almost every circumstance, but it does not rule out the possibility per se of some exception to the rule.

Third, the profession that a degree holder would enter after graduating generally requires professional licensure. This means that before beginning practice, the degree recipient must obtain additional authorization to begin practicing, which would typically flow from a government or standard setting organization. Like the second part, the third part requires licensure “generally,” which connotes that this rule will be followed in almost every circumstance, but it does not rule out the possibility per se of some exception to the rule.

In addition to the operative test, the definition also provides for an illustrative list of advanced degrees that are professional degrees and meet the definition. These degrees were codified by Congress into the definition as examples, meaning the Department does not need to do additional interpretive work to know that these specific degree programs qualify as professional degrees. Accordingly, the proposed rule designates each of the degrees on this list as a professional degree for purposes of eligibility for the higher Direct Loan Program limits.

The illustrative list of degrees also provides additional contextual clues that the Department may rely upon when discerning the facial or as applied meaning of the operative test to any specific degree program. For example, while the operative definition does not explicitly state that a degree must generally be at the doctoral-level to be considered a professional degree, the illustrative list of degrees suggests that this must be the case, as it contains only three non-doctoral degrees L.L.B. (a law degree no longer conferred by American institutions of higher education), as well as the two listed theology degrees (the M.Div. and the M.H.L.).[5]

In the same way, we assume that Congress does not write statutes in a vacuum, but rather “ legislates against the backdrop of existing law.” McQuiggin v. Perkins, 569 U.S. 383, 398, n. 3 (2013). Here, rather than charting a new course and writing a statute anew, without mooring to previously established statutes, Congress inserted a cross- reference to a long-established Department regulation that defines professional degree. In doing so, under the prior construction canon, we assume that the words and phrases in the definition that the Department has already given authoritative construction to, are to be understood as being adopted by Congress. See, e.g., Bragdon v. Abbott, 524 U.S. 624, 645 (1998) (“When administrative and judicial interpretations have settled the meaning of an existing statutory provision, repetition of the same language in a new statute indicates, as a general matter, the intent to incorporate its administrative and judicial interpretations as well.”); Sekhar v. United States, 570 U.S. 729, 733, 133 S. Ct. 2720, 2724, 186 L. Ed. 2d 794 (2013) (“[I]f a word is obviously transplanted from another legal source, whether the common law or other legislation, it brings the old soil with it.” (quoting Felix Frankfurter, Some Reflections on the Reading of Statutes, 47 Colum. L.Rev. 527, 537 (1947)).

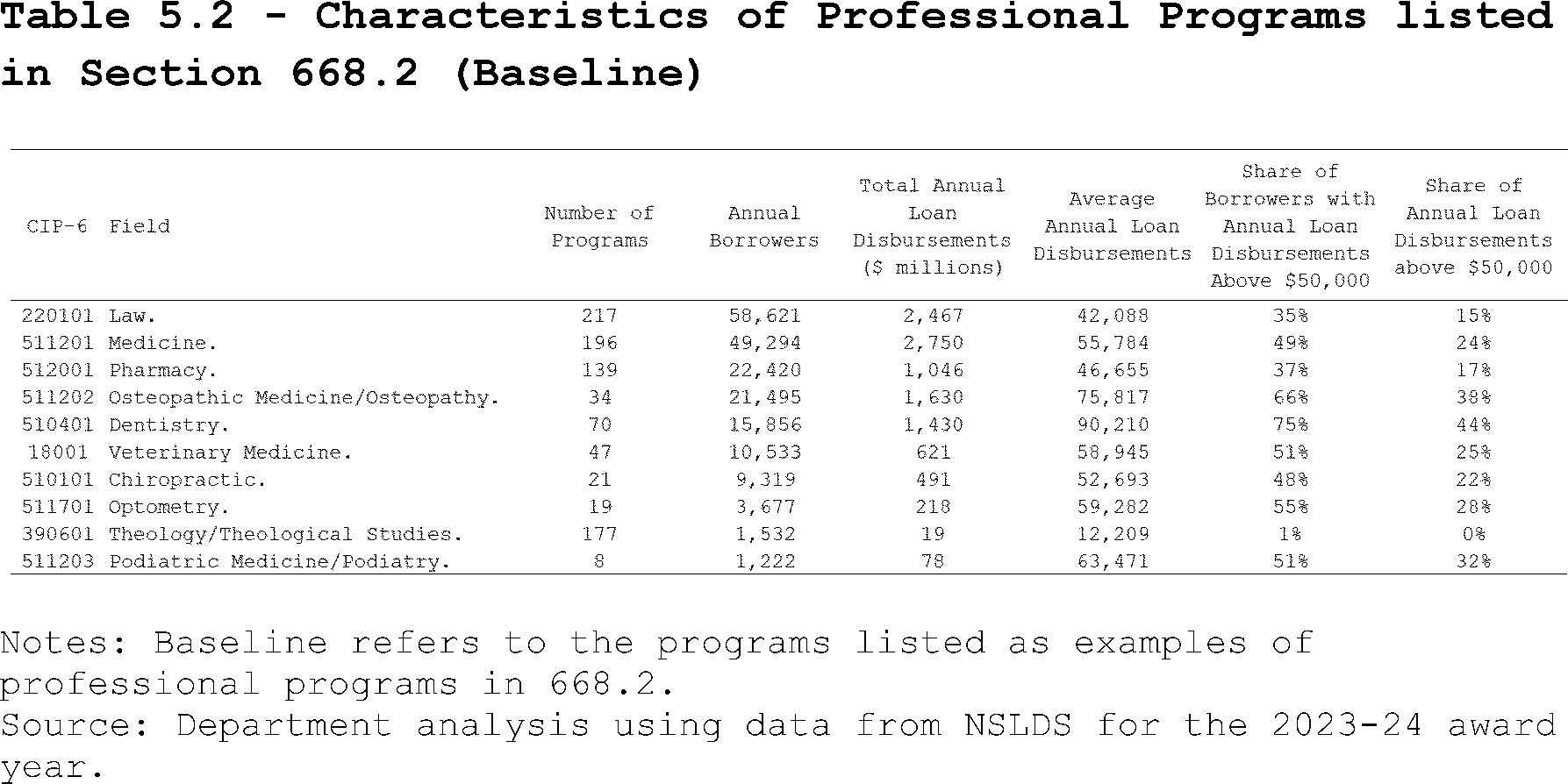

Against that backdrop, we explore the history of the adoption of the regulation in 34 CFR 668 to provide context as to what Congress implicitly incorporated into the OBBB. When the regulation was promulgated in 2007, the definition of professional degree in 34 CFR 668.2 was based on the long-standing definition of a first-professional degree used by the Department's National Center for Education Statistics (NCES). The 2007 Integrated Postsecondary Education Data System (IPEDS) Glossary defined first-professional degrees as meeting all of the following criteria: (1) completion of the academic requirements to begin practice in the profession; (2) at least 2 years of college work prior to entering the program; and (3) a total of at least 6 academic years of college work to complete the degree program, including ( printed page 4263) prior required college work plus the length of the professional program itself.

Additionally, at the time, NCES considered the first- professional degree as one which “encompasses certain occupationally specific and closely regulated degree programs including the following: medicine (M.D.), chiropractic (DC or DCM.), dentistry (D.D.S. or D.M.D.), optometry (O.D.), osteopathic medicine (D.O.), pharmacy (Pharm.D.), podiatry (Pod.D. or D.P.M.), veterinary medicine (D.V.M.), law (LL.B. or J.D.), and theology (M.Div., M.H.L., or B.D.)” ( Graduate and First-Professional Students: 2007-08, Susan Choy, et al, https://nces.ed.gov/pubs2011/2011174.pdf).

Prior to that, there had been little change in the criteria for first-professional degrees and in the 10 fields and accompanying degrees that NCES identified as specific examples of such degrees. Such criteria were used for reporting on such programs in IPEDS, and its predecessor survey, the Higher Education General Information Survey (HEGIS).

Against this backdrop, in defining professional degree in 34 CFR 668.2, in 2007, the Department proposed in the NPRM to add a definition of first-professional degree “based on the definition currently used by the National Center for Education ( sic) Statistics” (72 FR 44621). In response to a public comment requesting that the Department consider altering several definitions proposed in the NPRM, including first-professional degree, so that the terms used reflected the layman's language and terminology used in the Department's Federal Student Aid Handbook for student financial aid administrators, the Department agreed with the comment that it was not necessary to specify whether a professional degree is a first-professional degree for the title IV, HEA purposes, and the Department dropped the word “first,” but retained the term “professional degree” and made no changes to the definition proposed in the NPRM. (72 FR 62016). The definition of professional degree has not been further amended since November 1, 2007.

In overturning Chevron deference in Loper Bright Enters. v. Raimondo, 603 U.S. 369 (2024), the Supreme Court emphasized that Chevron had fostered “unwarranted instability in the law, leaving those attempting to plan around agency action in an eternal fog of uncertainty.” Id. at 411. The Court explained that Chevron had enabled administrative agencies to change course even when Congress had not authorized them to do so. Id. However, the Court did not abandon all reliance on agency interpretations of statute, explaining that interpretations issued by agencies “which have remained consistent over time, may be especially useful in determining the statute's meaning.” Id. at 370 (citing American Trucking Assns., 310 U.S. at 549).

Here, Congress adopted and codified an agency regulation that had been remarkably consistent over time, as it remained unaltered for nearly 20 years, and changes to it before then had been minimal. With that said, the regulation existed in a different context and served a different role in that it had no bearing on Federal student loan eligibility. In that sense, the rule existed in a paradigm where there were no significant legal consequences for a degree being counted, or not, as a professional degree. In addition to its longstanding nature, the comparative lack of legal consequences when the regulation was promulgated serves as some indicia of evidence that the interpretation represents a balanced and fair reading of what a professional degree is. The agency was, in promulgating the rule, free from outside pressure from students and institutions that have a financial incentive to insist upon a broader interpretation that includes more degree programs. While certainly not dispositive, these facts along with the Department's longstanding interpretation, provide “useful evidence in determining the statute's meaning.” Loper Bright, 603 U.S. at 370.

At the same time, by its own terms, the list of degrees in the definition need not be exhaustive and merely includes an illustrative list of degrees. The Department does not necessarily claim that the included list of professional degrees represents all professional degrees being offered by institutions, just those that the Department has identified as meeting the statutory definition. Indeed, the definition states that “Examples of a professional degree include but are not limited to” the degrees listed. This provides clear clues that the Department may, so long as the operative definition and context allow, add additional degrees to the list of professional degrees through regulation.

At the same time, context is key. And we are bound to adhere closely to the text of the statute. The interpretive canon noscitur a sociis is instructive in this context. It provides that words and phrases are “known by its associates,” or, when a word or phrase is “susceptible of multiple and wide-ranging meanings,” it is “given more precise content by the neighboring words with which it is associated.” United States v. Williams, 553 U.S. 285, 294 (2008). Here, the illustrative list of degrees Congress provided do just that; they provide context for the types of degrees that Congress considered to have met its definition of professional degree for the purposes of higher loan limits. So, the Department must consider what these degrees have in common and the context those commonalities provide. Id.

Degrees on the example list in 34 CFR 668.2 may be fairly compared to any degrees not on the list. If any given degree is similar to degrees on the list, that provides additional evidence that the degree at hand may be a professional degree. If any given degree is dissimilar to degrees on the list, that provides evidence that the degree at hand may not be a professional degree. Of course, this comparative exercise is not dispositive; the degree must also meet the bounds of the operative test of professional degree to be categorized as such. This exercise of running the degree through the operative definition, then comparing and contrasting it to the list of degrees cited in 34 CFR 668.2, appropriately takes into account the broader statutory scheme and ensures that the Department interprets the statute in accordance with the intent.

During the negotiated rulemaking process, members of the RISE Committee provided several examples of degree programs and certain fields for consideration as to whether those would qualify in the same general class as those programs stated as examples of professional degrees.

Several members of the Committee suggested the Doctorate in Clinical Psychology as another specific example of a professional degree program, noting that such programs meet all of the criteria in the definition of professional degree in 34 CFR 668.2. Additionally, they noted that, in the definition of qualifying graduate program in 34 CFR 668.2, Clinical Psychology programs are specifically included with other professional degree programs requiring postgraduate training to obtain licensure, including medicine (M.D.), dentistry (D.D.S. or D.M.D.), and osteopathic medicine (D.O.), and therefore are in the same class as these programs which are also specifically identified as professional degree programs.

Committee members also noted that a doctorate in Clinical Psychology is explicitly required for licensure to practice as a clinical psychologist in every state.

Further, several members of the Committee suggested using the Classification of Instructional Programs ( printed page 4264) (CIP) (a system originally developed by the Department's NCES for tracking and reporting fields of study and program completion activity) to identify additional degree programs that meet the definition of professional degree in 34 CFR 668.2. The CIP is an integral part of institutions' annual IPEDS data reporting of professional degree and other programs, as every postsecondary school that receives Federal student aid funds must use CIP codes to report their program data to the government. The CIP is the accepted Federal government standard on instructional program classifications and is used in a variety of education information surveys and databases, as well as by State agencies, national associations, academic institutions, and employment counseling services for collecting, reporting, and analyzing instructional program data.[6]

The CIP coding taxonomy, for instructional programs is organized on three levels: (1) A two-digit series of 48 general fields that groups a large number of related programs; (2) A four-digit series nested within each two-digit series which represent groupings of programs that have comparable content and objectives, within those two-digit fields; (3) A six-digit series which assigns unique six-digit codes to specific instructional programs. Six-digit CIP codes are the most specific program classifications under the taxonomy and institutions participating in the title IV, HEA programs are required to report completion data in IPEDS for each of their programs using the six-digit CIP code. Id, at 2. In some cases, instructional programs may be found in one or more series. For instance, a person can receive a degree in Statistics from a program that focuses on mathematical models; this program would be coded under code 27.0501 (Statistics, General). On the other hand, a person can receive a degree in Statistics from a program which focuses on the applications of statistical methods to the description, analysis, and forecasting of business data; this degree would be coded under code 52.1302 (Business Statistics).[7]

CIP codes generally apply to all levels of certificates and degrees. In some cases, however, degrees were specified in the examples for certain CIP codes in which Federal agencies needed to be able to obtain data on the number of degrees awarded in a particular field of study. For example, CIP code 51.1201 (Medicine) lists Medicine (MD) as an example.

The Doctorate in Clinical Psychology and each of the 10 fields and associated degrees identified in the definition of professional degree in 34 CFR 668.2 has a unique six-digit CIP code in the current CIP taxonomy. Members of the Committee suggested that the scope of the professional degree program defined in the proposed regulation include programs that meet the requirements for professional degree that are within the intermediate four-digit grouping of programs for each of these six-digit CIP codes, as assigned by the institution or determined by the Secretary. We agreed with the Committee members that such an approach would accurately include other advanced degree programs in these 4-digit intermediate CIP groupings that met all requirements for a professional degree as defined in 34 CFR 668.2. Under the proposed regulations, such advanced programs would be considered in the general class with the professional degree programs in Clinical Psychology and the fields and degrees identified in the professional degree definition.

The Department believes 4-digit CIP groupings are the most appropriate level for classifying programs for two reasons.

Specifically, NCES defines 2-digit CIP codes as “the most general groupings of related programs.” Comparatively, the 4-digit CIP series is defined as “groupings of programs that have comparable content and objectives.” [8] After examining the groupings, the Department believes that using 4-digit CIP groupings are closely related to the examples of professional programs listed in CFR 668.2 to qualify for the higher loan limits.

To provide an illustrative example, the proposed rule allows all programs with the 4-digit CIP code “01.80” to qualify for the higher loan limits. In this case, there is just one such program in the 4-digit CIP grouping 01.80: Veterinary Medicine. However, if all programs in the same 2-digit CIP family were used, programs that are not connected to a professional practice would be included, such as “Horticulture Science” (01.01.03), “Plant Sciences” (01.11.01), “Soil Chemistry” (01.12.02), “Brewing Science” (01.10.03), and “Dairy Science” (01.09.05), to name a few.

Veterinary medicine is categorically different from these other types of agricultural programs. The National Center for Education Statistics describes a veterinary medicine program as “a program that prepares individuals for the independent professional practice of veterinary medicine, involving the diagnosis, treatment, and health care management of animals,” while describing, for example, a horticultural science program as “a program that focuses on the scientific principles related to the cultivation of garden and ornamental plants, including fruits, vegetables, flowers, and landscape.” [9] Given the substantial difference in a program that prepares individuals to medically treat animals and a program that trains students on scientific principles related to gardening, the Department believed it would be illogical to include all programs sharing the same 2-digit CIP family.

In the Department's view, the explicit incorporation of a four-digit program CIP code into the regulatory definition of “professional degree” is not inconsistent with the statutory definition. Indeed, it would make explicit what is already implicitly a common element among the statute's illustrative examples of professional degrees. Furthermore, the CIP code taxonomy has administrative benefits for the Department and institutions given its wide use that make its use practically convenient. In sum, adopting this element would ease administrative burden and is consistent with the statutory framework.