Untangling deliverability, additionality and double counting related to renewable energy certificates for improved scope 2 emissions accounting

Published 23 April 2025 •

© 2025 The Author(s). Published by IOP Publishing Ltd

,

,

Citation Anders Bjørn et al 2025 Environ. Res. Lett. 20 051006DOI 10.1088/1748-9326/adc941

You need an eReader or compatible software to experience the benefits of the ePub3 file format.

Article metrics

1780 Total downloads

0 Video abstract views

Submit

Submit to this JournalDates

- Received 30 January 2025

- Revised 21 March 2025

- Accepted 4 April 2025

- Published 23 April 2025

Peer review information

Method: Double Anonymous

Revisions: 1

Screened for originality? Yes

Original content from this work may be used under the terms of the Creative Commons Attribution 4.0 license. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

The greenhouse gas (GHG) Protocol is the most widely used global standard for voluntary corporate GHG emission accounting and reporting (WBCSD/WRI 2004, Walenta 2021). Initially developed in 2001 through a multistakeholder process with heavy industry involvement, the standard has since been updated and elaborated multiple times. A central concept within the standard is the organization of corporate emissions into direct (scope 1) and indirect emissions, with the latter category further divided into point-of-generation emissions from purchased and consumed electricity, heating, cooling, and steam (scope 2) and all other indirect emissions (scope 3). With corporate electricity consumption accounting for around 15% of global GHG emissions (Schäfer et al 2025), scope 2 emissions are a central component of most company’s GHG accounts. Since 2015, the GHG Protocol has permitted companies to report scope 2 emissions through purchases of renewable energy certificates4 (RECs) (GHG Protocol 2015) (box 1). Each REC purchase allows a company to report zero scope 2 emissions for 1 MWh of its electricity consumption as if the company is physically supplied by the renewable generation facility that they bought the REC from. Since then, companies have greatly increased their RECs purchases and RECs have come to play an important role in companies´ reporting on progress against net-zero targets (Bjørn et al 2022, 2025, Ruiz Manuel and Blok 2023, Langer et al 2024).

Box 1. Summary of the GHG protocol´s existing scope 2 accounting rules (GHG Protocol 2015, Bjørn et al 2022).

Under the GHG Protocol, companies are required to report their scope 2 emissions using both market- and location-based (LB) accounting. Market-based (MB) accounting allows companies to use RECs to claim the use of renewable electricity and report the emissions from its production, rather than the emissions of the electricity mix they physically consume. At a given site and year, a company calculates MB electricity emissions (E) by, first, multiplying the part of their electricity consumption covered by the REC (CREC) by the emission factor of the REC (EFREC, usually zero) and, second, multiplying any uncovered electricity consumption (C–CREC) by a residual grid mix emission factor (EFres), which represents the local grid without the electricity generation that has been claimed by RECs:

Under LB accounting, all companies on a grid simply multiply their electricity consumption (C) by the average emission factor (EFaverage) for the grid mix, regardless of whether they have purchased RECs:

In a grid with no RECs sales, EFres is equal to EFaverage. In a grid with REC sales, EFres is always higher than EFaverage, with the difference depending on the volume of REC sales relative to total renewable electricity production (Klimscheffskij et al 2015, Paris et al 2024).

While the GHG Protocol requires companies to report both market- and LB scope 2 emissions, it allows companies to choose one of the two accounting approaches when setting and tracking progress against an emission reduction target.

The role of RECs in the 2015 standard has been criticized by academics, consumer protection organizations, market analysts and media for potentially leading to poor and even misleading emission accounting and claims (Bloomberg 2024, The Guardian 2024). In Europe, there has been a big focus on companies thousands of kilometers away buying RECs from Norwegian hydropower plants, even though they cannot be physically supplied by power from these plants, the plants were built many years before the RECs market was created, and local Norwegian companies are also reporting the climate benefit of the hydropower (Mulder and Zomer 2016, Paris et al 2024). In the US, which has seen a massive recent expansion in photovoltaic capacity, an additional line of criticism is that the annual accounting steps of the 2015 standard allow companies to make the counterintuitive claim that they are fully powered by photovoltaic, even at night (De Chalendar and Benson 2019). These concerns can be largely summarized as (1) lack of physical connection between the corporate REC buyer and renewable energy source, (2) not causing additional renewable generation, and (3) double-counting.

We observe that actors frequently confuse these three accounting issues in discussions related to the upcoming revision of the GHG Protocol’s standard for scope 2 (GHG Protocol 2023b). At worst, this entanglement of accounting issues could lead to a new standard that does not fully address all of them.

In this comment, we argue that the 2015 standard suffers from all three accounting issues, and that each issue requires its own solution. First, we present the three accounting issues in more detail. Second, we argue why they should be seen as distinct, despite some level of interdependence. Third, we outline promising approaches for solving each accounting issue.

1. The illusion of connection: lack of deliverability

Under the 2015 standard, a company may ‘match’ its electricity consumption with RECs from generators it is not physically connected to and, when physical connectivity is present, the company may temporally mismatch its electricity consumption (e.g. at night) with purchased RECs (e.g. from photovoltaics). This violates the basic rule within the attributional accounting approach (which the GHG Protocol’s Corporate Standard purports to be based on) that activities included in a company´s GHG inventory must be physically connected to the company (Brander 2022, Brander and Bjørn 2023). So, while it is generally impossible to trace the actual supplier of a given MWh consumed by a company from the common grid, making emission claims based on RECs purchased from generators that cannot physically deliver power to the company clearly goes against good inventory accounting practices.

The root cause behind the lack of deliverability is that the 2015 standard allows RECs to be traded within geographical areas that are larger than the areas in which physical electricity is traded5 and that the standard suggests the use of annual time steps by default, even though power is typically consumed rapidly after it is generated.

2. Taking credit without deserving it: lack of additionality

Under the 2015 standard there is no requirement for a causal relationship between the reporting company and the zero-emission factor that each purchased REC allows it to use when calculating its market-based scope 2 emissions. This is problematic for two reasons.

Firstly, from an attributional accounting perspective, even if there is time and location matching, there will not be a rationale for claiming to ‘be powered by’ one single specific generation technology, out of the multitude that may be dispatching power at the time and location of consumption. Reporting the emission rate associated with a specific generator will only be accurate if the company can show that it caused the power from a specific generator to exist, i.e. prove additionality (Brander and Bjørn 2023).

Secondly, from a pure impact perspective (which goes beyond questions of accuracy in attributional accounting (Brander 2022)) there is no point in purchasing RECs that do not cause an increase in the deployment of renewables or reduce emissions. It is clearly misleading if large publicly facing companies can use RECs to give the impression that they are progressing well against their net-zero targets without actually reducing power emissions and instead effectively shifting these emissions to other electricity customers who are under less pressure to report emissions reductions, such as small companies and individual households (Bjørn et al 2022).

3. When emissions do not add up: double counting

In theory, the 2015 standard ensures that the market-based scope 2 emissions of all electricity consumers in a region sum to the region´s total power emissions, by not counting the zero-emission attribute of a given MWh of renewable energy generation more than once. This balance should be achieved through the residual emission factor, which represents a grid´s average emission factor adjusted upward to exclude the renewable energy production covered by sold RECs (box 1). For example, while Norway´s average emission factor in 2022 was 7 gCO2 per kWh, its residual emission factor was 502 gCO2 per kWh (Paris et al 2024).

In practice, however, companies often resort to using average emission factors as proxies when residual factors are not available (GHG Protocol 2023a, Stachelscheid and Dutzi 2025), hence benefiting from the zero-emission attribute of renewable energy production already counted in the sold RECs. A second source of double counting is when companies only report either market-based emissions or location-based emissions, instead of following the dual reporting requirement of the GHG Protocol (box 1) (Paris et al 2024, Stachelscheid and Dutzi 2025)6. In both cases, even in a situation where all power consumers (companies, households, etc) report their scope 2 emissions, the sum of these reported emissions will underestimate total power emissions.

4. Interdependent but distinct issues

The frequent confusion between the three accounting issues presented above may be partially explained by the fact that there is a level of correlation between them, whereby one issue is more likely to occur if another issue is present. For example, lack of deliverability has been blamed for causing lack of additionality, as the former allows companies in regions with REC scarcity (e.g. Germany) to buy low-cost RECs from regions with surplus RECs (e.g. Norway) (Mulder and Zomer 2016, Paris et al 2024), and it allows companies that consume electricity in hours with low renewable energy generation to buy low-cost RECs tied to power produced in hours with surplus production (Google 2020, Ricks et al 2023). Lack of geographical deliverability has also been seen as enabling double counting in situations where companies do not follow the dual reporting requirement (box 1), with German companies using Norwegian hydropower RECs to report low market-based emissions, while Norwegian companies also benefit from the zero-emission attributes of hydropower in their location-based emissions (Paris et al 2024). Double-counting may also decrease the likelihood of additionality since companies that use low average emissions factors to report market-based scope 2 emissions, instead of higher residual emission factors as required by the standard (box 1), have less incentive to buy RECs. In turn, this means they do not help to drive the level of REC scarcity required for meaningful price signals to renewable project developers (Paris et al 2024).

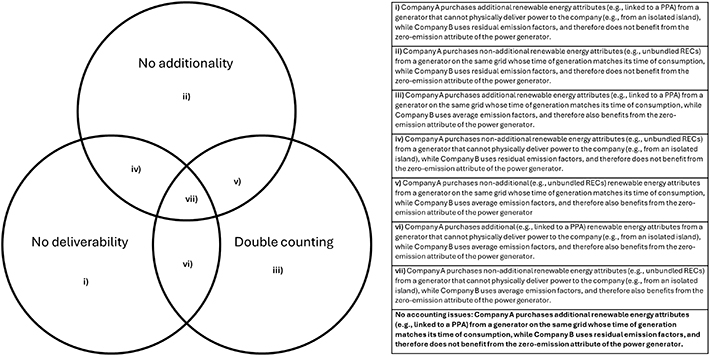

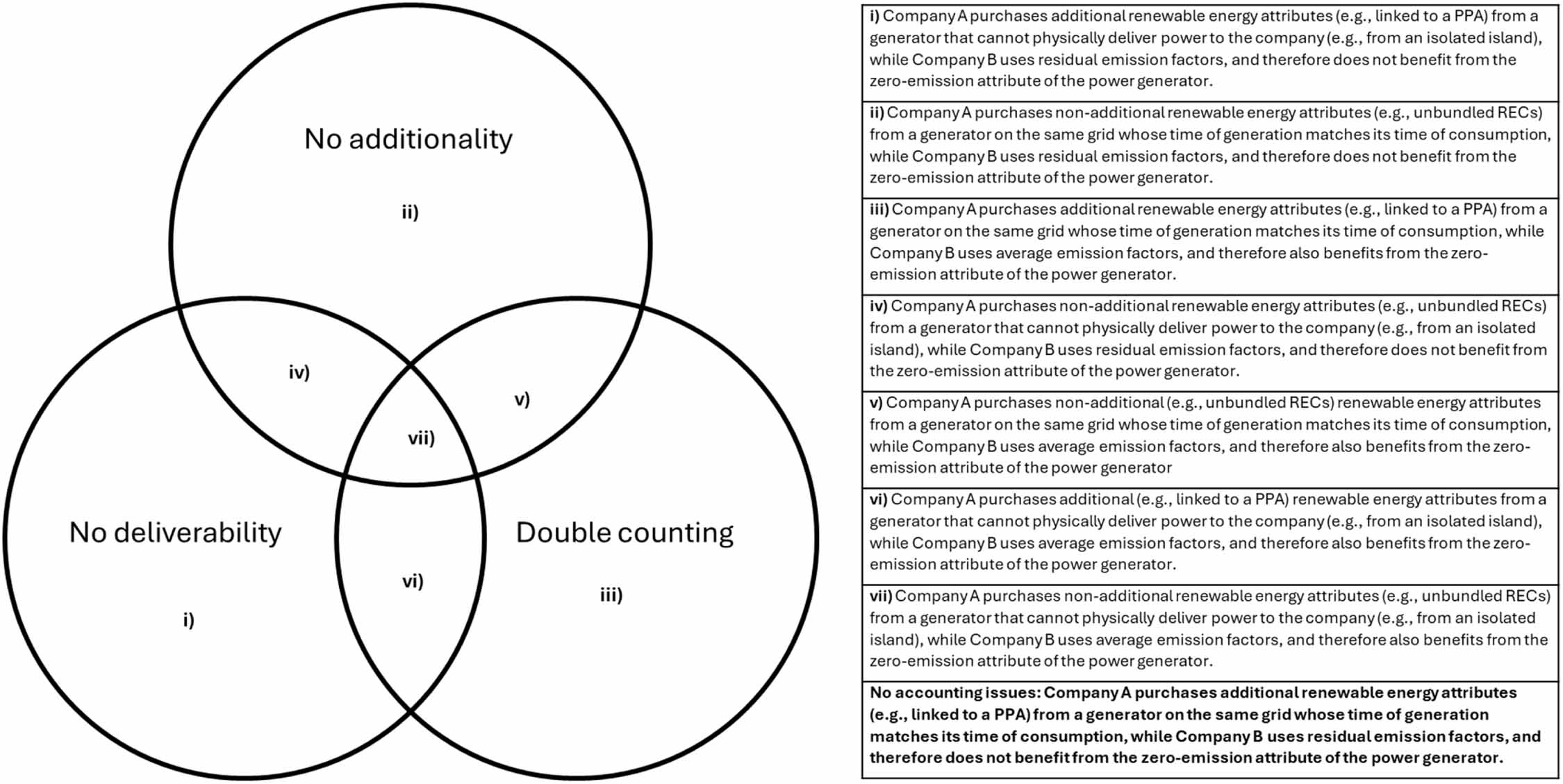

However, correlation is different from causation. For example, as shown by Galzi (2023) for the case of France, we should not assume that an accounting solution that ensures geographical deliverability also ensures additionality. Likewise, temporal deliverability does not necessarily ensure additionality, as it is possible for a company to buy RECs from facilities whose time of production matches the time of consumption without causing these facilities to exist. In fact, all seven combinations of the three accounting issues are plausible (figure 1).

Figure 1. Illustrative scenarios for the seven combinations of the three accounting issues. All cases involve two companies co-located on the same grid. PPA = power purchase agreement.

Download figure:

Standard image High-resolution image{kind=link}

5. Potential solutions to each accounting issue

Deliverability may be ensured by recent proposals for companies to buy RECs matched to the hour and location of consumption, while similarly using local and hourly residual emission factors for the unmatched part of the power consumption (Google 2020, GHG Protocol 2023b). Such restrictions would recognize the local and (in the absence of storage) short-lived nature of electricity. While hourly RECs and the corresponding hourly average and residual emission factors are just starting to emerge (Electricity Maps/Flexidao 2024, Soria and Barraza 2024), a recent study found that many companies are already seeking RECs originating from the same country (Bjørn et al 2025), hence indicating that companies may find it practically feasible to restrict their REC sourcing to the same grid.

Additionality tests have been implemented within voluntary carbon credit markets for decades and some of these tests are also suitable in the context of scope 2 accounting (Schäfer et al 2025). For example, an investment test involves a financial simulation of the renewable energy project issuing the RECs with the goal of understanding whether the project would not have been financially viable in the absence of the RECs market, or in the absence of a power purchase agreement, if such an agreement exists. Still, more research is needed to understand the practical applicability of additionality tests by corporate REC buyers and other actors.

Avoiding double-counting is largely a matter of ensuring that all companies comply with the existing GHG Protocol requirement (GHG Protocol 2015) of reporting both location-based and market-based scope 2 emissions and calculating the latter based on residual emission factors (box 1). For this, accurate residual emission factors must be calculated for each grid and, potentially, hour (Klimscheffskij et al 2015, Electricity Maps/Flexidao 2024). Further, to prevent companies from cherry-picking an emission accounting approach in connection with their climate target, the GHG Protocol could require companies to set climate targets for both market-based and location-based scope 2 emissions, instead of allowing them to either set location-based or market-based targets (box 1).

6. Outlook

When discussing potential revisions to emission accounting rules (GHG Protocol 2023b), it is crucial to first clearly articulate what the issues with the current accounting rules are. We argue that there are three interrelated but distinct issues with the 2015 scope 2 standard (GHG Protocol 2015) and, further, that these accounting issues must be solved separately. The accounting solutions outlined in this Perspective should inform the revision of GHG protocol standard, along with considerations of the practical implications for companies and other actors. These discussions are also relevant for emerging emission accounting standards related to ‘green fuels’ (Ricks et al 2023, Langer et al 2024) and for scope 3 accounting, where RECs and other environmental attribute certificates also play a role (Holzapfel et al 2023).

Acknowledgment

This research was funded by Innovation Fund Denmark, Grant 2122-00084B (A B and C H G).

Data availability statement

No new data were created or analysed in this study.

Conflict of interest

The first author is a remunerated member of the Technical Council of the Science Based Targets initiative. The other authors declare no competing interests.

Footnotes

- 4

Here, we use REC as an umbrella term for all environmental attribute certificates used globally in the context of scope 2 accounting, including guarantees of origin and certificates linked to power purchase agreements (PPAs), following Bjørn et al (2022).

- 5

The GHG Protocol does not define individual geographical REC markets and instead leaves this task to regional REC program operators. For example, the Association of Issuing Bodies defines 30 European countries as a single REC market.

- 6

This points to the separate issue that there is currently no entity systematically verifying claims by companies that they have calculated their reported emissions in accordance with the GHG Protocol.

- The University of Liverpool

- City University of Hong Kong (CITYU): Department of Physics

- Lawrence Livermore National Laboratory